EAGLE COMPLIANCE, LLC

Business Consulting

July 22, 2024

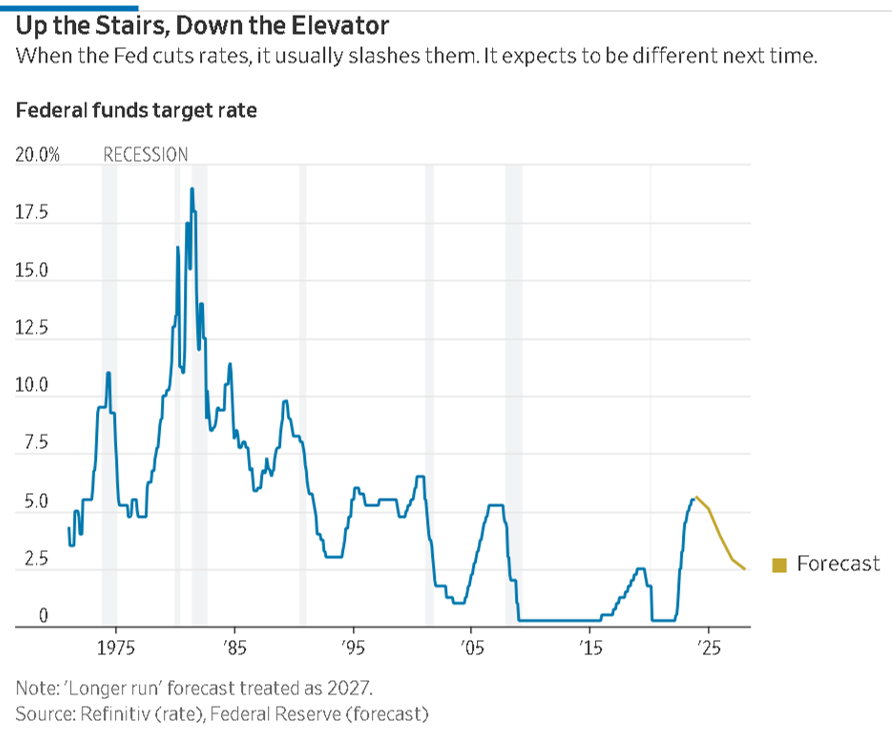

Rate Cut Coming, Just Not Now

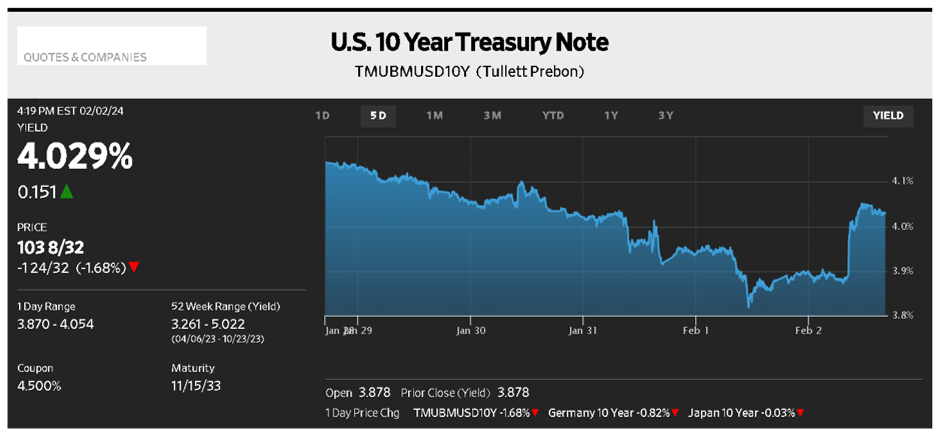

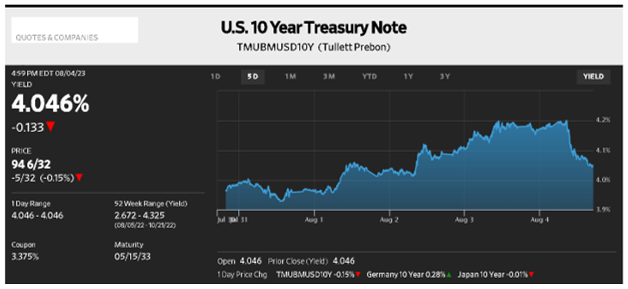

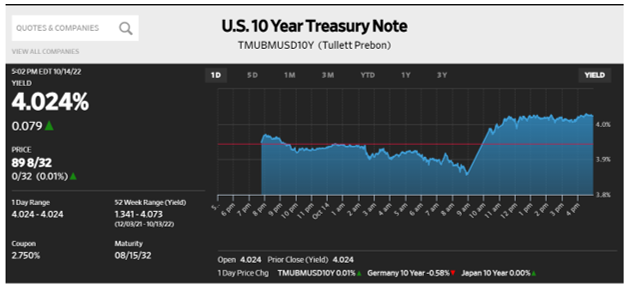

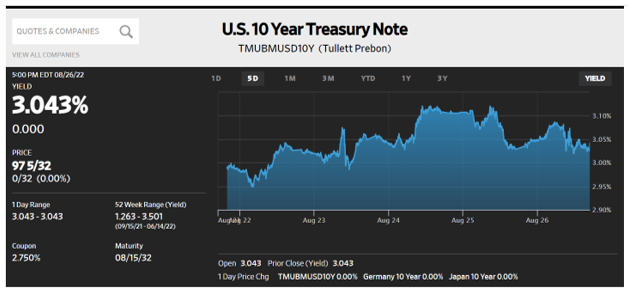

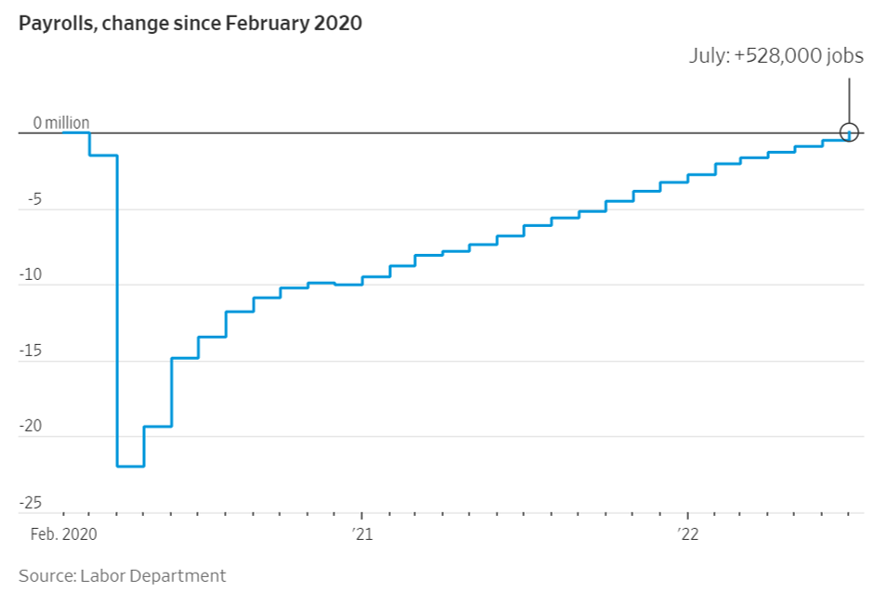

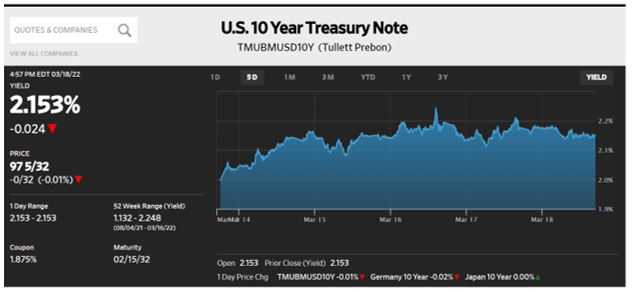

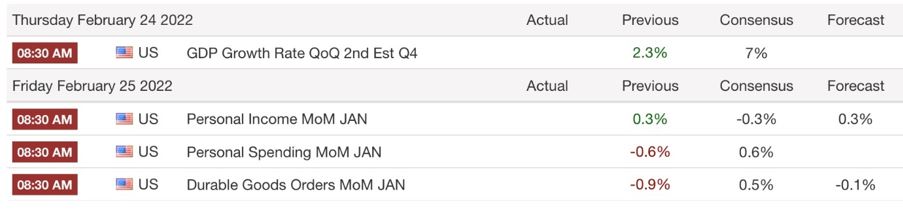

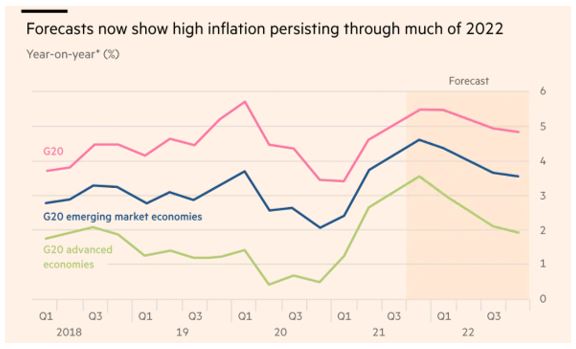

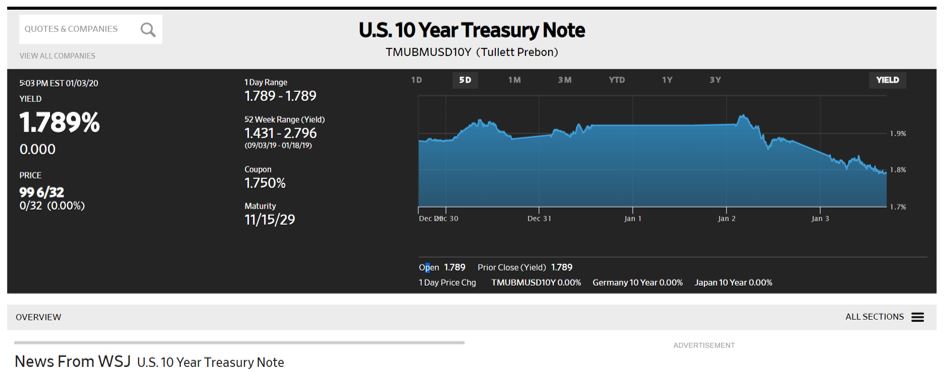

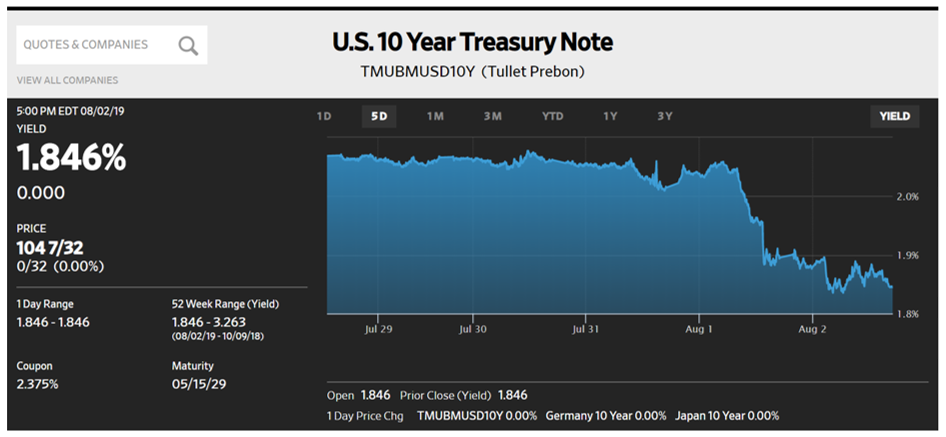

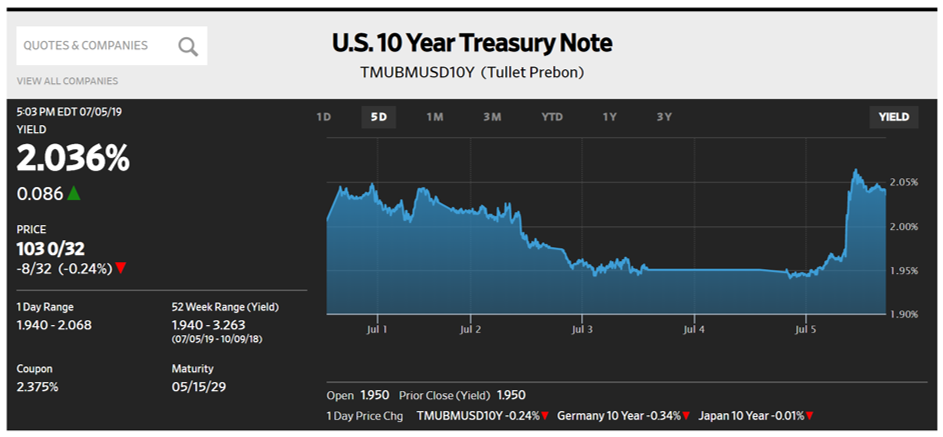

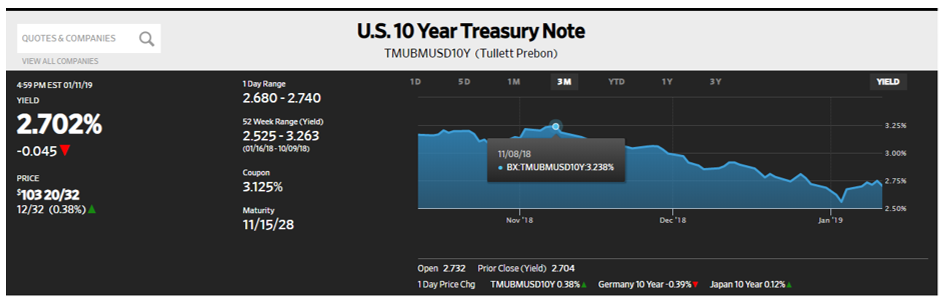

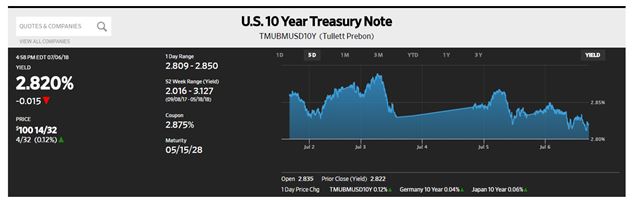

That was the message from Chairman Jay Powell last Monday in a speech before the Economic Club in Washington DC. “I’m not going to be sending any signals one way or another on any particular meeting. We’re going to make these decisions meeting by meeting.” That captures the consistent theme of the Chairman but after reports of a tighter labor market and improving inflation data the market has a 2% chance of a rate cut at the conclusion of the July 30-31 meting but a 98% chance after the September 17-18 meeting which is the last one before the November 5 election.

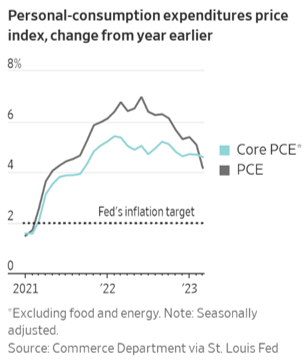

Support for that view could come this Friday with the Fed’s preferred inflation gauge expected to show core PCE flat at 0.1% and down 0.1% y/y to 2.5%.

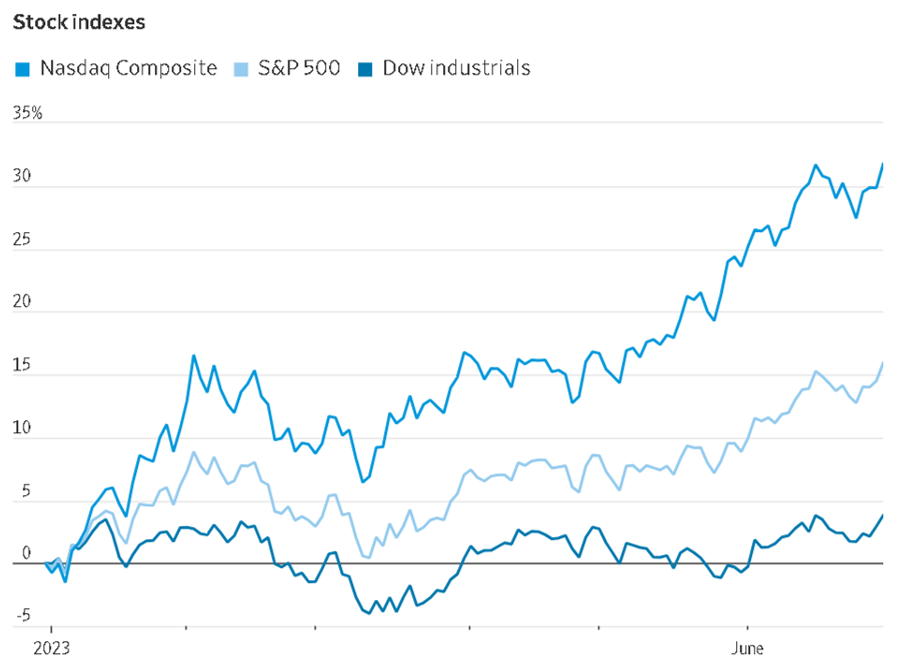

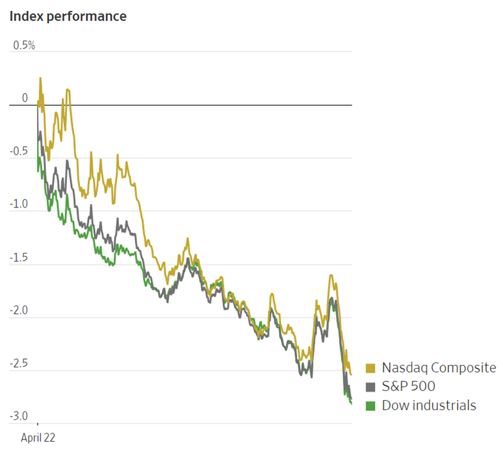

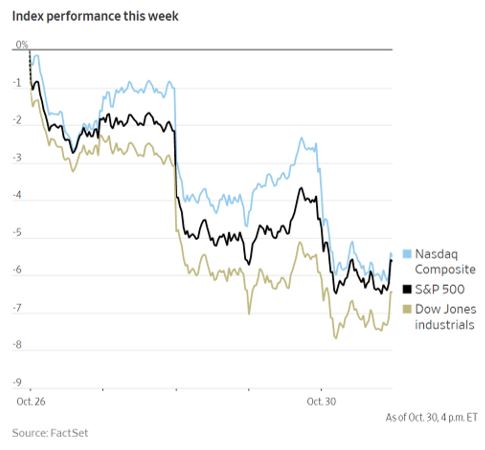

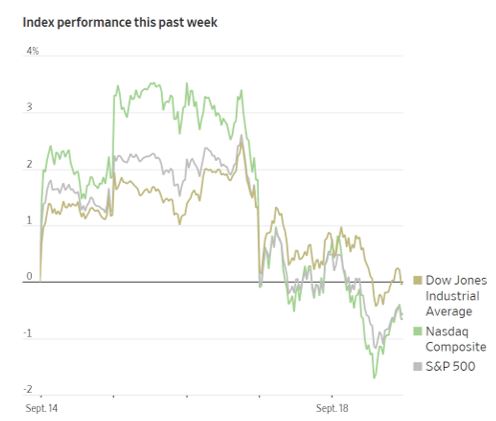

Anticipation of that news did little for the markets last week as the DJIA was the only major index to show a gain while the S&P 500 was down 6% and the tech heavy Nasdaq dropped 3.6%. Their down week was already in place before CrowdStrike, a provider of malware and virus protection software filed a system update that knocked out service to millions of Microsoft Windows users affecting banks, media services, and airlines. On the day, CRWD was down 11.10%.

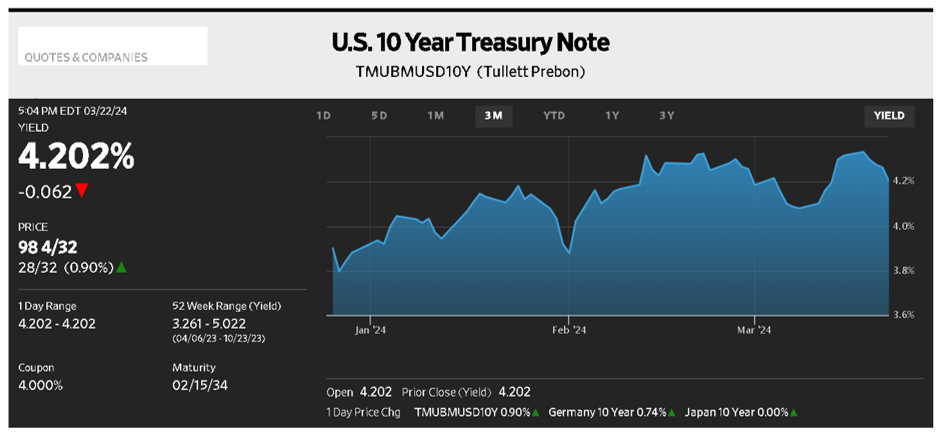

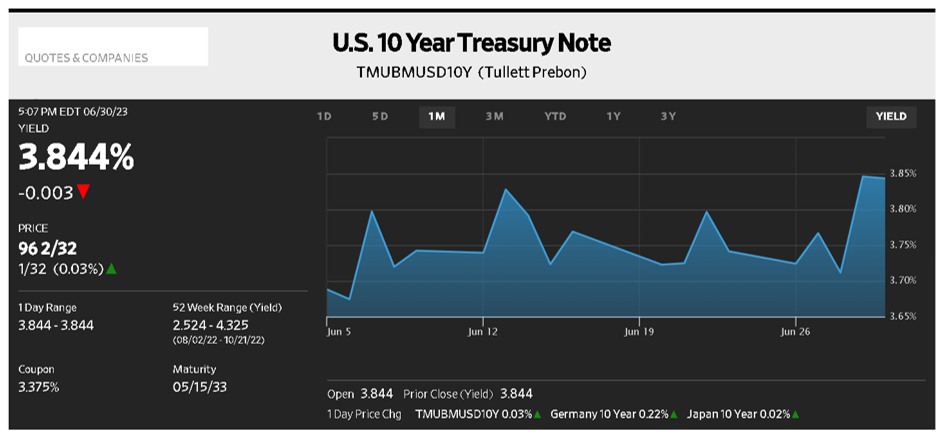

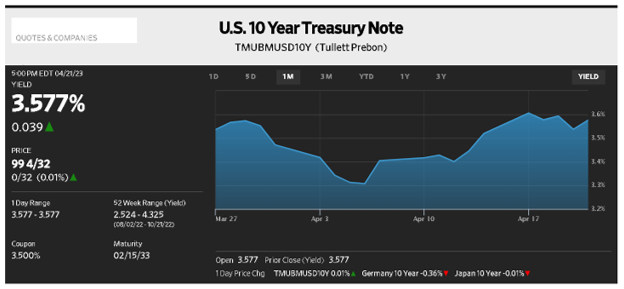

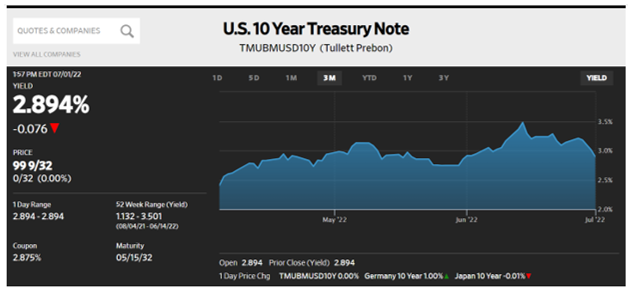

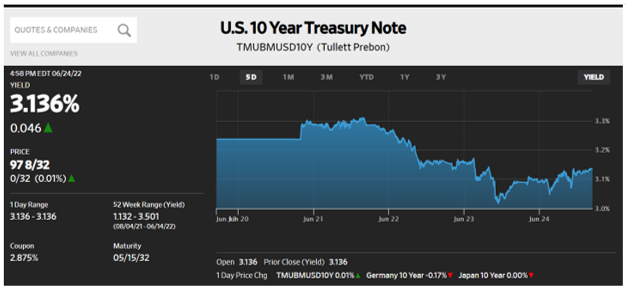

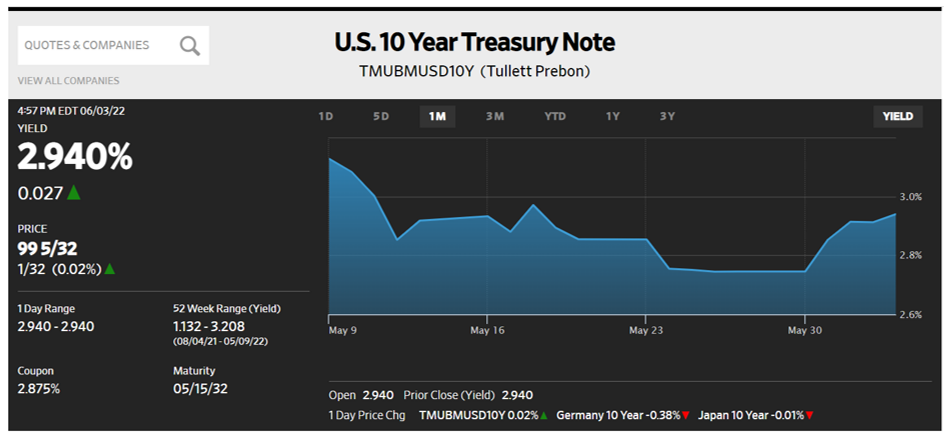

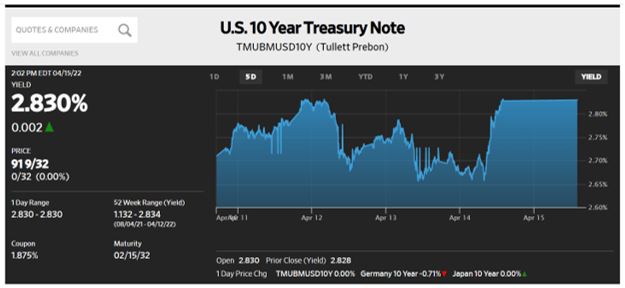

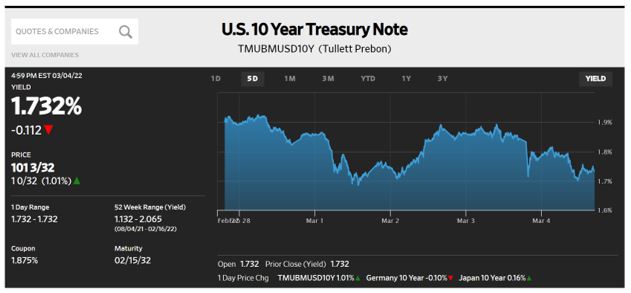

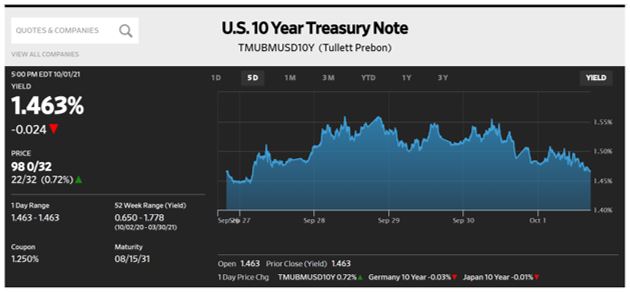

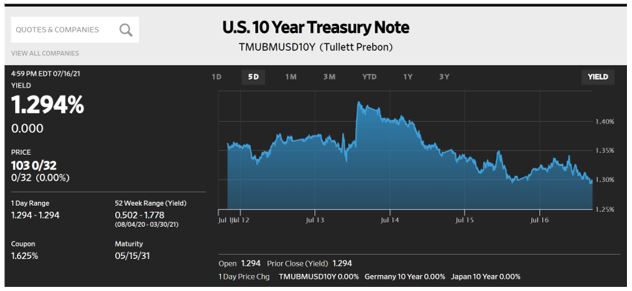

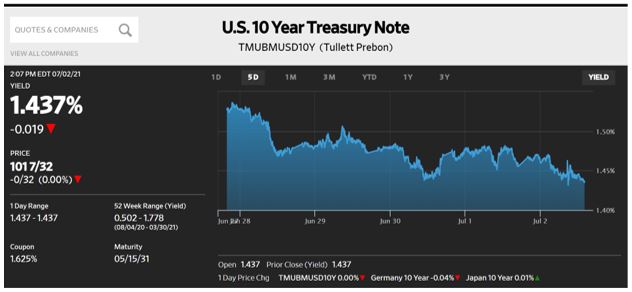

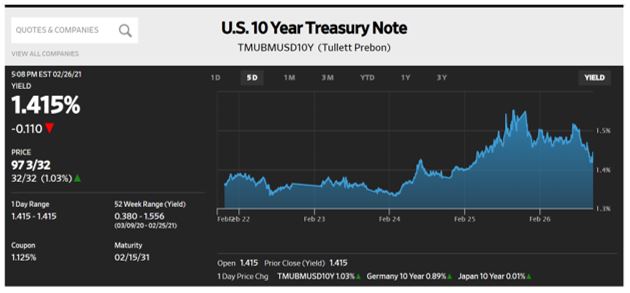

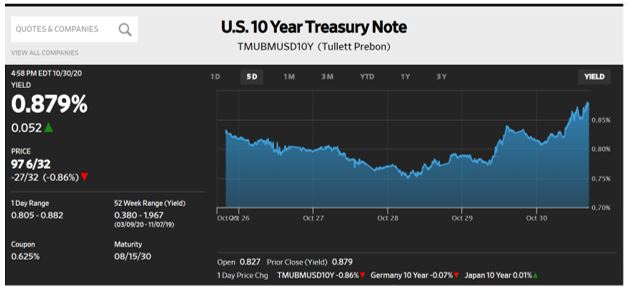

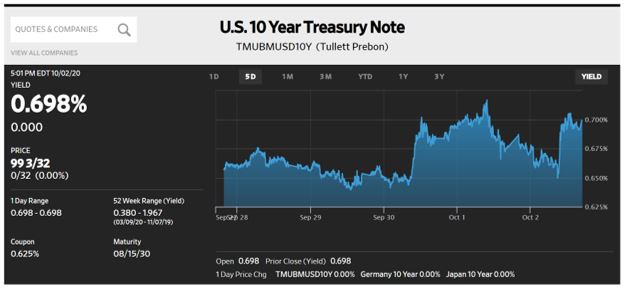

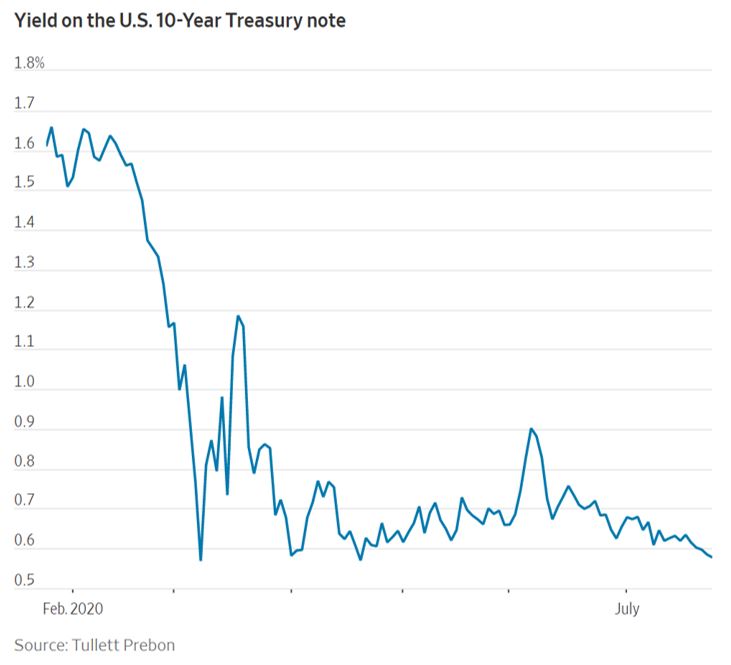

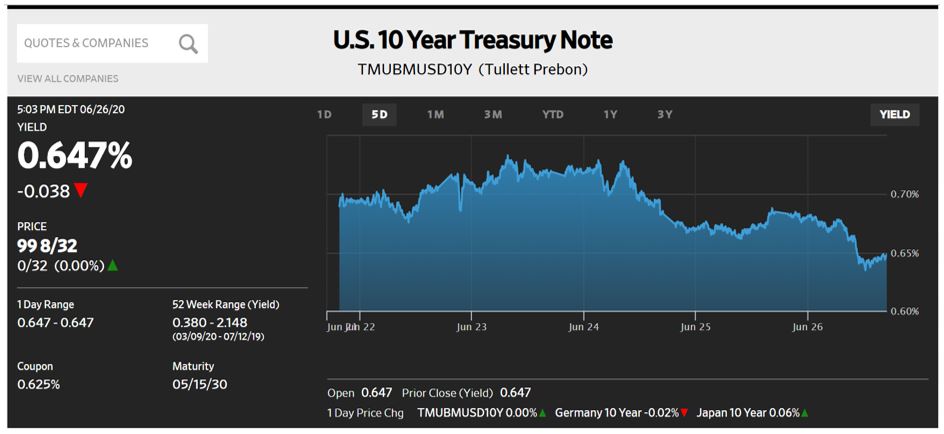

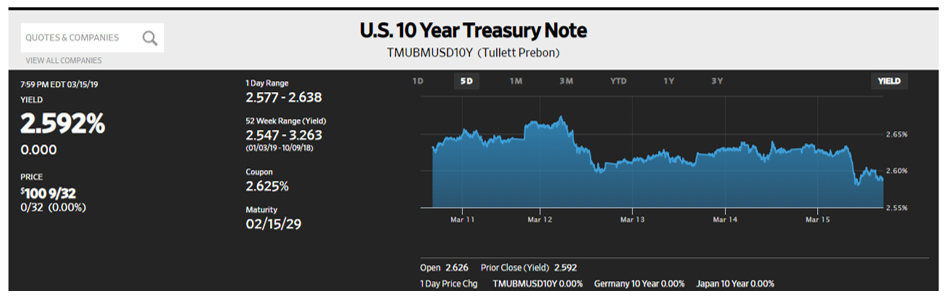

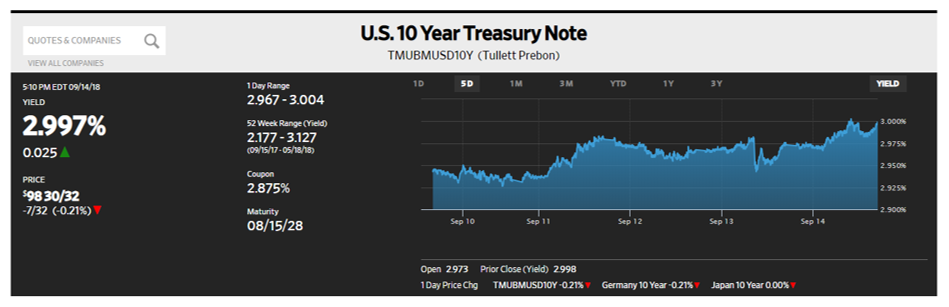

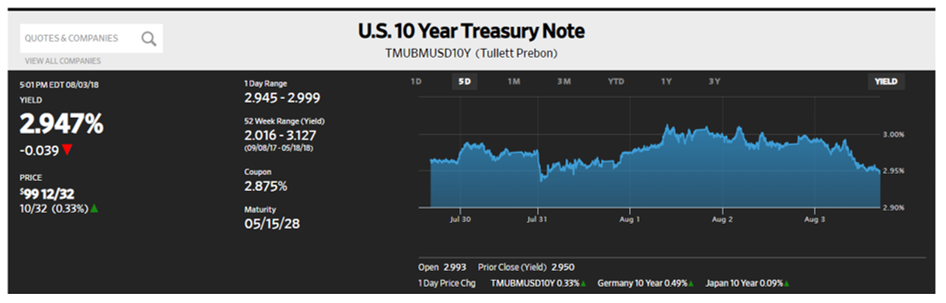

Rates didn’t fare much better as a mid-week move to 4.15% couldn’t hold and the benchmark ten-year note faded to 4.24% on Friday, 6 bps higher than when the 504 programs July debentures were priced.

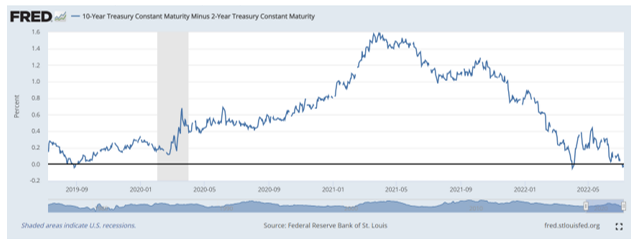

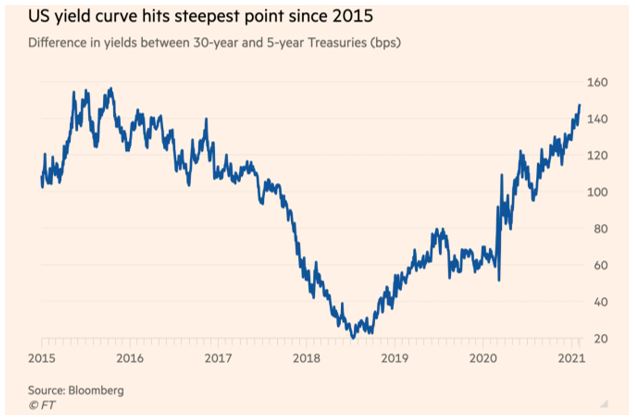

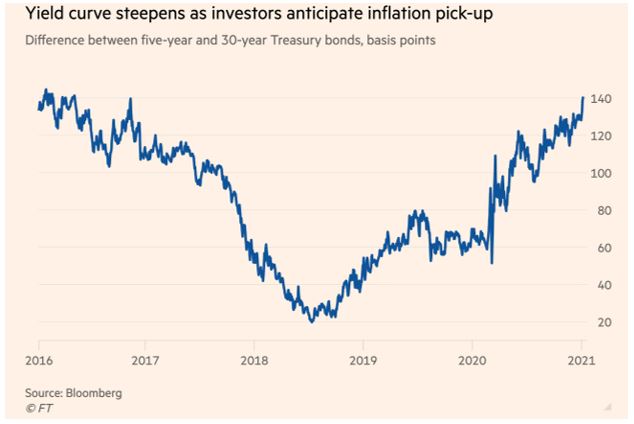

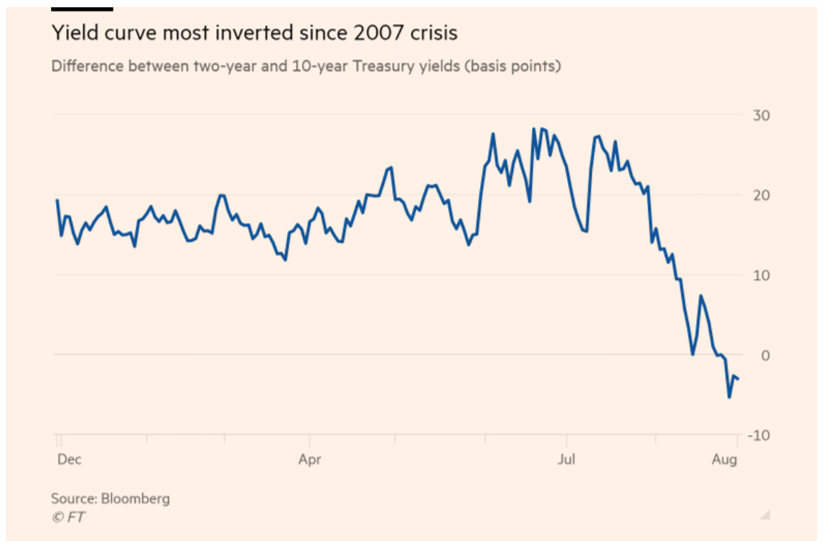

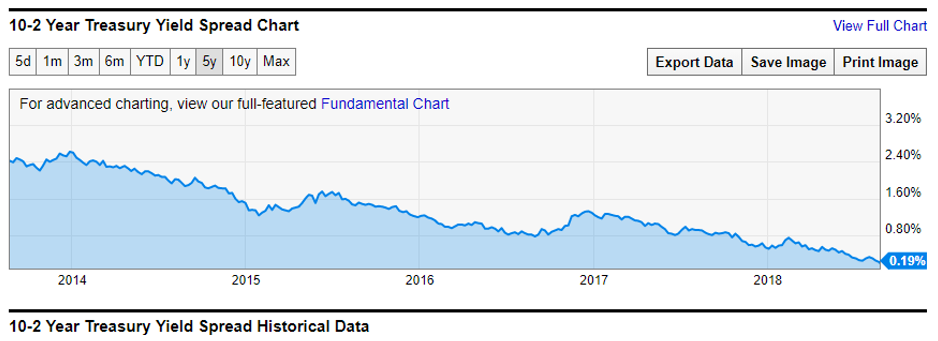

As ten-year rates have declined slightly since the June 27 Presidential debate short-term rates have outperformed in what market participants call the “Trump trade” because if elected, tax cuts are expected to be extended and pro trade tariffs introduced. Combined with probable interest rate cuts and an increased need for Treasury financing the result should be a steeper yield curve. Since the debate the 2/10 curve has moved from -49 bps to -28 bps.

Hard to Rollover

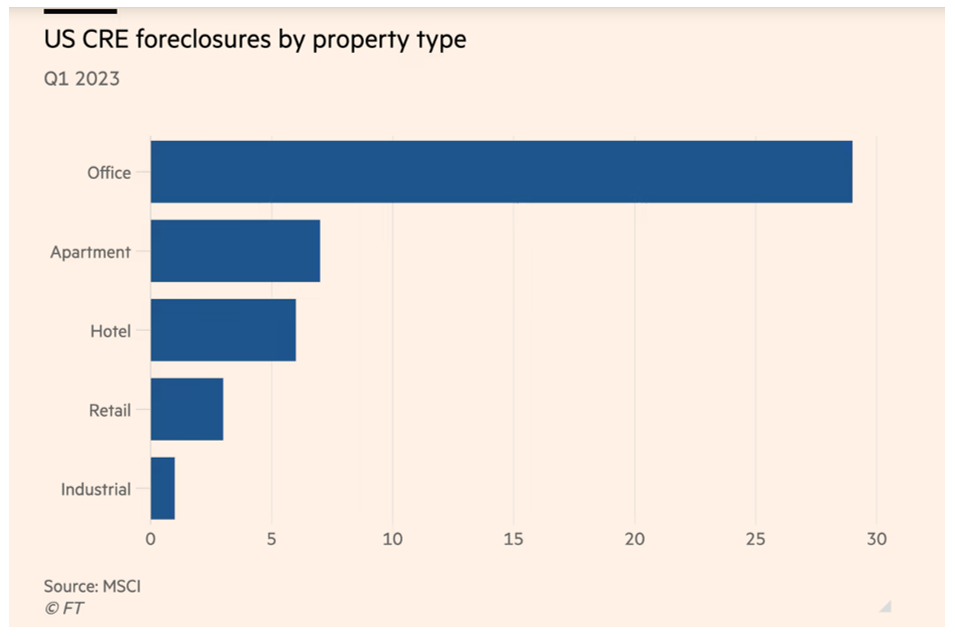

It is estimated that as many as $260 billion commercial real estate loans, many of which had triple-A ratings, are coming due in a higher rate environment with tighter credit conditions. Their category is SASB (single asset, single borrower) and was considered very safe as evidenced by their bond rating. A WSJ article states the rate of loans at or near default has nearly tripled over two years to 8.7% in 2024.

The article noted the financial models behind the ratings never forecast property prices falling below the value of the debt but the pandemic, higher interest rates, and a work from home environment has resulted in many near vacant buildings.

The Week Ahead

No Fedspeak in the blackout period ahead of the FOMC meeting, an active week for Treasury with 2Q2024 GDP plus Personal Income and PCE.

Monday – Treasury sells $146 billion 13 & 26 week Bills.

Tuesday –Treasury sells $69 billion two-year Notes, Existing Home Sales.

Wednesday –Treasury sells $70 billion five year Notes and $30 billion two-year FRN’s, New Home Sales.

Thursday – Treasury sells $44 billion seven year Notes, 2QGDP forecast at 1.9%, Durable Goods estimate is 0.6%.

Friday – Personal Income expected to decline to 0.4% and core PCE forecast at 0.1% and 2.5% y/y.

July 15, 2024

A Matter of Focus

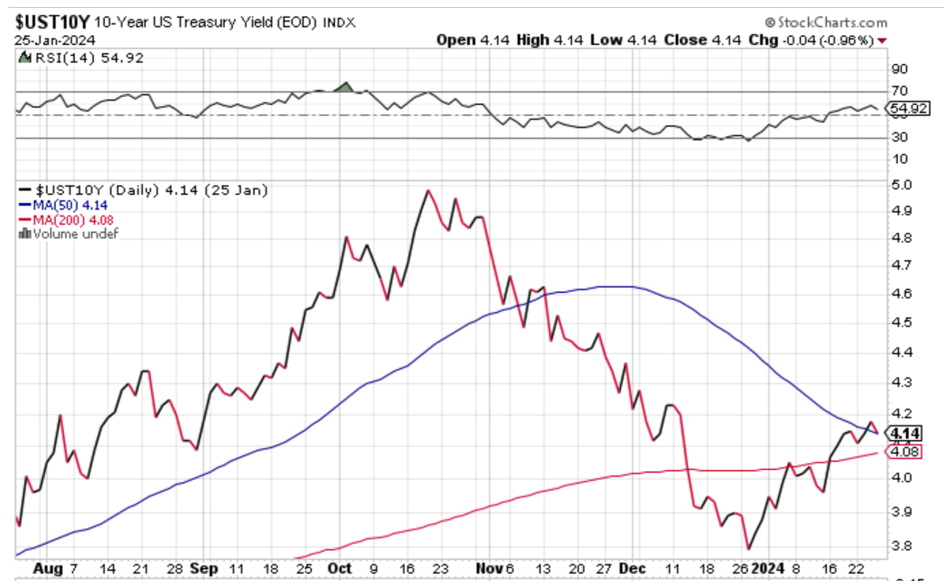

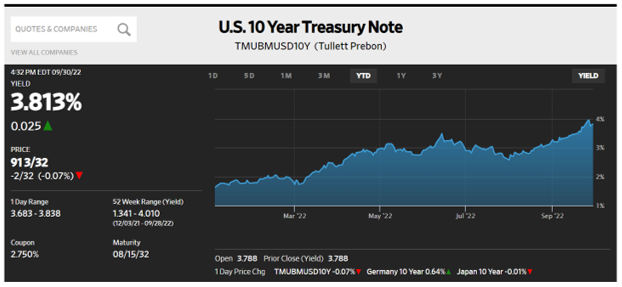

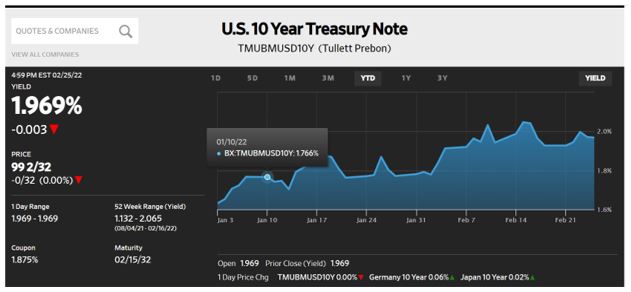

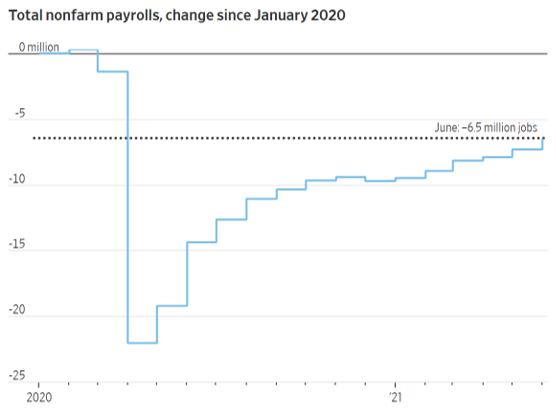

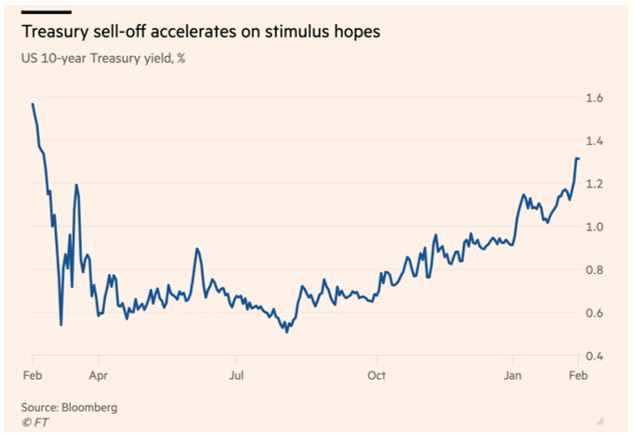

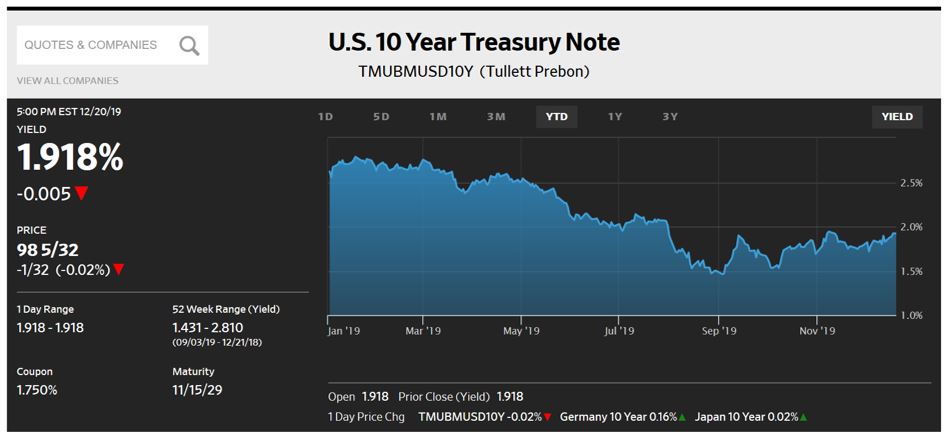

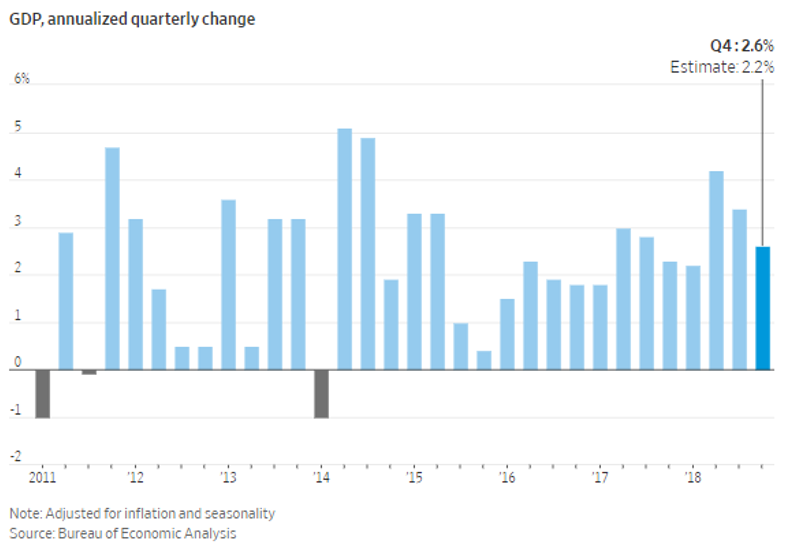

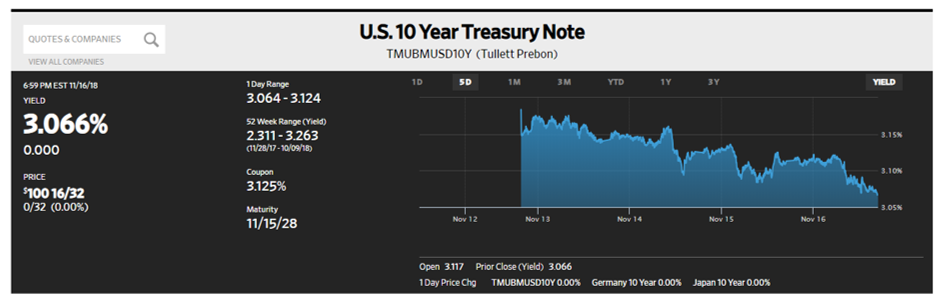

As we moved through the July 2024 Debenture offering market conditions stabilized and then improved significantly the morning of pricing with the release of the June CPI report. On Tuesday and Wednesday of the week FOMC Chairman Powell testified before the House Financial Services Committee. In his commentary, he walked a delicate line, reiterating fear that lowering interest rates too late or too little could put the economy and the labor market at risk, while recognizing that cutting rates too soon or too much could equally stall or reverse the disinflationary progress already achieved. He was clear that more good data was needed to instill the needed confidence to justify a rate cut, but he also emphasized that the FOMC was ready and willing to respond if it witnessed unexpected weakening. Market participants who have been, and remain, anxious for the Fed to adjust policy sooner rather than later choose to largely focus upon the “ready and willing to respond” portion of the Chairman’s comments. Last Friday’s Non-Farm/Employment report revealed significant downward revisions in the labor market; that data coupled with Thursday’s release of the CPI report (unexpected 0.1% decline for June (1st monthly decline since May 2020) and CPI year-over-year at 3.0%) was enough to convince market participants that a rate cut by the FOMC in September was all but a done deal. By late morning Thursday, the probability of a July rate cut remains a minimal 9%, while the probability of a rate cut in September was priced in at 85% (see charts below, updated through Friday, July 12, 2024) and 10-Year Treasury Notes rallied to yield 4.17%.

Investor response to the $7.9 million 10-Year, $17.4 million 20-Year, and $469.4 million 25-Year 504 offerings was quite positive and resulted in spread narrowing from initial indications on all issues: on the 10-Year from +65 bps to +63 bps, on the 20-Year from +73 bps to +71 bps and on the 25-Year from +73 bps to +71 bps. Light new issue competing supply in the agency commercial mortgage-backed-securities market was again a contributing factor. The July debenture rates of 4.75% for the 10-Year and 4.89% for both the 20-Year and 25 Year are the lowest debentures rates priced since May of 2023. The 25-Year rate is 50 bps under the program life average of 5.39% and the spread over Treasury (+71) continued to contract (2 bps m/m) and was 8 bps below its program life average of T+79. Participation by various investor types was spread evenly, a healthy sign for the program with money managers, insurance companies, and banks continuing to participate, reinforcing the diversity of the account base for the 504 program.

The Week Ahead

Monday - Treasury sells $146 billion 13 & 26 week Bills

Tuesday - Business Inventories (May), Import Price Index (June), Export Price Index (June), NAHB Housing Mkt Index (July)

Wednesday - Treasury sells $13 billion 20-year Bonds, Industrial Production (June), Capacity Utilization (June), Housing Starts (June), Building Permits (June), Beige Book

Thursday - Treasury sells $19 billion 10-year TIPs, Initial Jobless Claims, Philadelphia Fed Business Outlook Index (July)

July 8, 2024

Revisions Rule

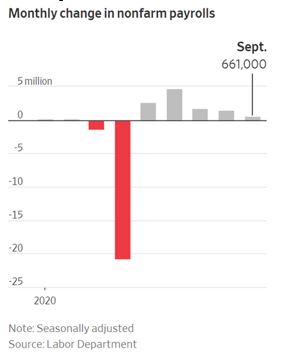

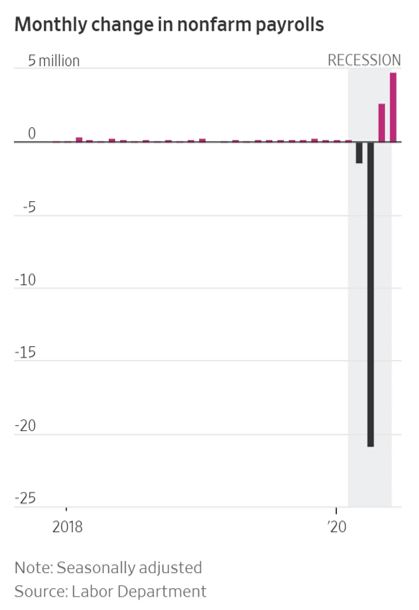

Downward revisions of 111,000 for April and May offset the higher than expected 206,000 number for June’s job growth allowing the bond market to push rates lower and keeping stocks at their record highs.

After a poor reaction to the previous week’s consensus level PCE data that pushed rates higher by 20 bps a weaker than expected ISM Services number, plus a weak Factory Orders number helped rates recover ahead of Friday’s report which should lend support to a September rate cut. Post the jobs report trade activity was muted due to the holiday weekend, but even though there has been little follow through to recent inflation and jobs data the trend is encouraging as economic activity is slowing in response to higher interest rates and a slightly tighter jobs market.

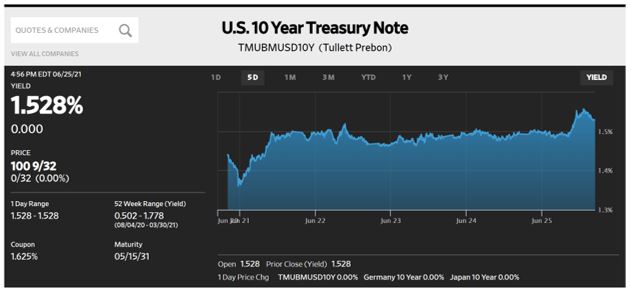

At 4.28% the benchmark ten-year Note is just 3 bps below where the June 504 debentures were priced and credit spreads in the ACMBS market remain stable.

Jobs

Job creation continues to be driven by the Health Care, Government and Travel & Leisure sectors that have been responsible for 1.7 million of the 2.7 million jobs created over the last year. In addition to unemployment rising to 4.1% the 3.9% average hourly earnings increase y/y was the smallest since 2021 and is another indication the economy is cooling as inflation improves.

These considerations will not force the Fed to act before they are assured inflation will not reignite and that was mentioned by Mary Daly, President of the San Francisco Fed and voting member of the FOMC, “I don’t want to pull up too short or too early and then have inflation stay high. That’s a terrible, terrible situation. I refuse to do that.”

The Week Ahead

A busy week with active Fedspeak as Chairman Powell appears before Congress, the quarterly Treasury refunding, and more inflation data that should be helpful.

Monday –Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – 504 program announces its July debenture sales, Treasury sells $58 billion three-year Notes, Jay Powell testifies before the Senate.

Wednesday – Treasury sells $39 billion ten-year Notes, Jay Powell speaks to the House.

Thursday – 504 program prices its July debentures, CPI forecast at 0.1% and 3.1% y/y, Treasury sells $22 billion thirty year Bonds.

Friday – PPI forecast at 0.1% and 3.2%.

July 1, 2024

Unexpected

After marking time while waiting for Friday’s Personal Income and PCE data the market got consensus level numbers and shrugged them off. Personal Income came in at 0.5%, a bit higher than expected and the PCE price index was 0.0% (down from 0.3%) and 2.6% y/y, down 0.1%. Market reaction disinverted the 2/10 curve to -35 bps as CT-10 moved 12 bps higher on the week to close at 4.39% with more supply in that maturity not due until next week.

It does seem unusual that with a 72% probability of a rate cut at the Fed’s September meeting the rate for the ten-year benchmark is 42 bps higher since January 1.

With that inflation data out of the way the market will now wait for this holiday shortened week to provide jobs data on Friday after a JOLTS report (Job Openings and Labor Turnover Survey) on Tuesday and the ADP private payroll figures on Wednesday. These reports may complement the improving inflation data to influence the Committee as it receives more PCE data just ahead of its next meeting on July 30-31, though no action is expected at that meeting. As mentioned, the September meeting is targeted as it is the last meeting before the November 5 election.

Other Data

- The Conference Board reported an uptick in Consumer Confidence after a downward revision.

- Durable Goods orders were 0.1% vs. 0.7% in April.

- 2Q2024 GDP was revised to 1.4%.

- Case Schiller Home Price Index was +0.4% and 7.2% y/y.

- - New Home Sales were sharply below consensus at 635K annualized.

Those last two items illustrate continued price appreciation and mortgage rates above 7% are central to a Morgan Stanley report that identifies two thirds of all outstanding mortgages have a rate less than 4% creating a “lock in” effect for homeowners to stay put to enjoy their low cost of finance while benefitting from accumulated price appreciation.

This Harvard University chart shows the gap that has resulted from higher interest rates over the last four years reducing supply and limiting affordability in a sector of the economy that normally accounts for 3-5% of US output.

The Week Ahead

Some Fedspeak, including Chairman Powell, a light week for Treasury and Friday’s jobs report for anyone not enjoying a long holiday weekend.

Monday – Treasury sells $140 billion 13 & 26 week Bills, ISM Manufacturing report.

Tuesday – Jay Powell speech in Portugal.

Wednesday – Factory Orders expected to be 0.3%.

Thursday – Happy Independence Day!

Friday – Non-Farm Payroll forecast at 195,00 with 4% Unemployment.

June 24, 2024

A Quiet Week

A holiday shortened week left bonds and stocks pretty much where they started the week with some economic reports, Retail Sales in particular, affirming some concern about consumer spending. At 0.1% with April revised down to -0.2% spending was curtailed by high prices even though the price of gasoline declined $.14 per gallon to $3.45. Analysts attribute this weakening trend to a cautious consumer looking for relief from high interest rates.

Another indication of consumer caution is the third consecutive month of declining Existing Home Sales that were down 0.7% on the month and 2.8% y/y. High mortgage rates (6.87%), low inventory, and rising prices are the cause of this conundrum for home buyers. This National Association of Realtors chart shows the national median price of a home to be $419,300 in May, a 50% increase from when the pandemic began in March 2020. That four-year increase almost doubles the 27% increase in existing sale prices for the four years prior to the pandemic and illustrates the cumulative impact of inflation resulting from a 525 bps increase in the cost of money.

As quiet as last week was, this week contains the potential for some volatility with the second revision for 1QGDP and Friday’s release for Personal Income and Personal Consumption Expenditures. The latter is the Fed’s preferred inflation gauge and is expected to decline monthly and y/y.

The Week Ahead

Heavy Fed speak and Treasury issuance with PCE on Friday and Consumer Confidence reports from both the Conference Board and the University of Michigan.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – Consumer Confidence from the Consumer Board and Treasury sells $69 billion 2-year Notes.

Wednesday – Durable Goods and Treasury sells $70 billion 5-year Notes and $28 billion 2-year TIPS.

Thursday – Jobless Claims, second revision of 1QGDP expected to be 1.3%, and Treasury sells $44 billion 7-year Notes.

Friday – Personal Income expected to increase to 0.4% and PCE forecast at 0.0% and 2.6% y/y, U of M Consumer Confidence survey.

June 17, 2024

Dot Plot vs. Data

Starting with the May CPI numbers that were modestly better than expected, Wednesday was an active day for the markets as the Fed did as expected by announcing no change to policy, but with a hawkish tone to the announcement and Chairman Powells’s press conference. Their “dot plot” projects just one rate cut for 2024, down from three when last disclosed in March, but the rates market assigned a 64% chance of two cuts this year anyway and that optimism reduced the benchmark ten-year rate by 11bps to 4.32%.

That leads to the short term vs. long term perspective that identifies the difference in the Fed’s “dot plot” projections and what the market expects. Since policy is data dependent the Fed plan may change but whether there is one or two cuts this year the longer term projection of nine rate cuts over three years is unchanged.

| Year | Previous | Current |

|---|---|---|

Thursday’s PPI report was sharply lower than expected with the May number at -0.2% vs. a +0.1% consensus and with the y/y rate of 2.2% also lower than expected. That pushed the bond rally further to 4.24%, a closing level not seen since March 30, and through the 50 and 200-day Moving Averages for the benchmark. Here is the end of week close, 20 bps lower on the week and reflective of how the market is more focused on data than a dot plot.

The next FOMC meeting ends July 31 and though there is an 88% probability there will be no rate cut the market now expects there will be at least two by year end. There will be three CPI reports before the September 8 FOMC meeting that is the last one scheduled before the November 5 election, so that meeting is attracting attention for a potential policy change for obvious reasons.

Fifteen of nineteen FOMC members expect the Fed will cut rates this year and that group is evenly split between one and two cuts, meaning the next three CPI reports and PCE reports will be crucial for policy decisions.

Other Central Banks

- Bank of Japan has announced it plans to significantly cut back its bond buying program as it unwinds its easy money policy while reducing its balance sheet. Compared to the overnight funds rate in the US of 5.25-5.50% the BoJ rate is zero to 0.1%.

- Bank of England Policy Committee meets Thursday with central banks in Australia, Norway and Switzerland also meeting.

The Week Ahead

Fed speak has resumed, a light calendar for reports and Treasury.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – Treasury sells $13 billion 20-year Bonds, Retail Sales forecast at 0.2% and Industrial Production consensus is 0.4%.

Wednesday – Federal holiday for Juneteenth.

Thursday – Treasury sells $21 billion 5-year TIPS.

Friday – Manufacturing PMI is released.

June 10, 2024

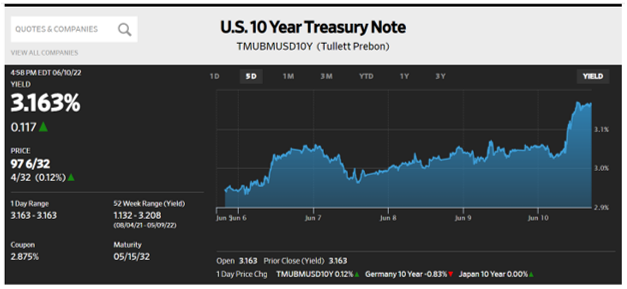

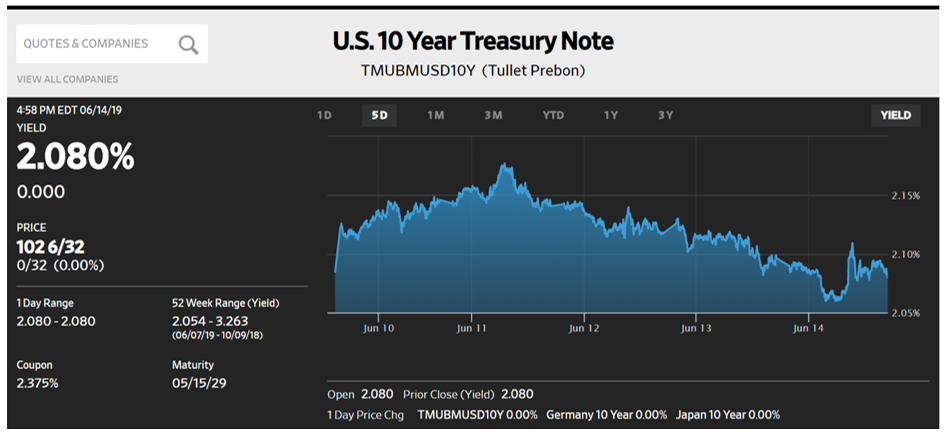

Market conditions were favorable, and improved, as we moved through the June 2024 504 debenture offering. The Thursday prior to the announcement 10-Year Treasury Notes yielded 4.56%. However, subsequent releases of a mildly weaker consumer spending report, an as expected Personal Consumption Expenditures report (little progress in the Fed’s Fight Against Inflation), and a weaker ISM Manufacturing Index report (45.4 vs. an expected level of 49.5 (a 3-month low)) caused Treasury yields to decline significantly. At pricing (following Thursday morning) the 10-Year Treasury Note yield had declined 25.5 basis points to 4.305%. This despite comments from several Fed officials including Minneapolis Fed President Neel Kashkari that “many more months of positive inflation data, I think, [are needed] to give me confidence that it’s appropriate to dial back [policy]”; and despite the impending release of the closely watched U.S. employment report due out the following morning. That report proved stronger than expected as nonfarm payrolls rose by 272k in May, surpassing the 180k gain expected marking the largest gain in two months. This caused an immediate upward spike in interest rates (see chart below). The good fortune of having priced the June 504 offerings 1-day earlier saved small business borrowers approximately 12 bps.

Investor response to the $16.4 million 20-Year and $388.5 million 25-Year 504 offerings was quite positive and resulted in spread narrowing from initial indications on both issues; on the 20-Year from +78 bps to +75 bps and on the 25-Year from +75 bps to +73 bps. Light new issue competing supply in the agency commercial mortgage-backed-securities market was certainly a contributing factor. The June 25-year debenture rate, at 5.04%, was 20 bps below May. The rate is 35 bps under the program life average of 5.39% and the spread over Treasury (+73) continued to contract (2 bps m/m) and was 6 bps below its program life average of T+79. It was pleasing to observe that spread-driven money managers who had recently expressed mild concern over narrowing spreads purchase almost 40% of the 25-Year offering. These buyers are typically very competitive and vigorously analyze investment alternatives.

June 3, 2024

As Forecast, Mostly

The event of the week was Friday’s Personal Income and PCE report that came close to forecast, helping interest rates recover and for stocks to close the month in positive territory.

Personal Income was 0.3% and 2.7% y/y with the core reading also unchanged at 2.8%. What was lower than expectations was Personal Spending. At 0.2% it was below its forecast of 0.3% and down from 0.7% in April with analysts speculating consumers are showing the effect of years of inflation on their savings.

This Factset chart shows the decline in the Chicago Purchasing Managers survey with its current weak reading of 35.4 in May almost matching its recent low during the pandemic.

Additionally, this report followed Thursday’s second revision of 1Q2024 GDP at 1.3%, down from its previous reading of 1.6% with expectations it could drop even lower.

Neither the PCE report nor a regional PMI report will cause any change in policy at the June 12 FOMC meeting, but they do reflect signs of a consumer slowdown which could complicate Fed policy decisions. Friday’s jobs report will be the next significant report ahead of that meeting.

A Poor Start to the Week

Hawkish Fedspeak and weak demand for almost $184 billion of two, five, and seven year Treasury Notes began the week by pushing rates higher as fears of a more restrictive Fed took hold. The benchmark ten-year Note yielded as much as 4.61% before closing the week at 4.50%. This risk off attitude carried over into stocks as the market assigned a slightly better than 50% chance of a rate cut in September, the Committee’s last meeting before the November 5 election.

Inverted Curves & Recessions

The Treasury curve inversion that began four months after the Fed began raising rates in March 2022 was expected to herald a recession, but analysts now are questioning how accurate that concept is. This Federal Reserve Bank of St. Louis chart shows the curve’s status at -68 bps but with consistent job growth and 1Q2024 GDP at 1.3% risk of a recession has been fading. Though GDP has been declining, Friday’s jobs report is expected to match the April number of 175,000 with the unemployment rate unchanged at 3.9%.

Recent weakness in equities seems as much related to markets being overpriced as to an economic slowdown but identifies why the bank is being cautious about cutting rates while inflation remains above its target level. Some Fed officials like Neel Kashkari, President of the Minneapolis Fed, suggest the neutral rate may be higher than it was before the pandemic and the market could tolerate a higher rate than 5.50%. That balance of selecting a rate that neither spurs nor slows growth is the dilemma faced by the Fed.

The Week Ahead

Fedspeak takes a pause ahead of the FOMC meeting, the 504 program prices its June debentures, a light week for Treasury, and the jobs report is the main event.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – 504 program announces its June debenture sale, Factory Orders forecast at 0.7%.

Wednesday – ISM Services expected to increase.

Thursday – 504 program prices its June debentures, Jobless Claims expected to be flat at 216,000.

Friday – Non-Farm Payroll consensus is 175,00 with unemployment unchanged at 3.9%.

May 28, 2024

Reduced Volatility

A quiet week leading up to a holiday weekend ahead of the next piece of inflation data on Friday. PCE is what the Fed watches most closely and is expected to decline to 3.7% y/y. Both equities and rates moved sideways with the rates markets seeing reduced supply and a light number of economic reports. Closing the week at 4.48% the ten-year benchmark is flat with where it was for the 504 program’s May debenture pricing.

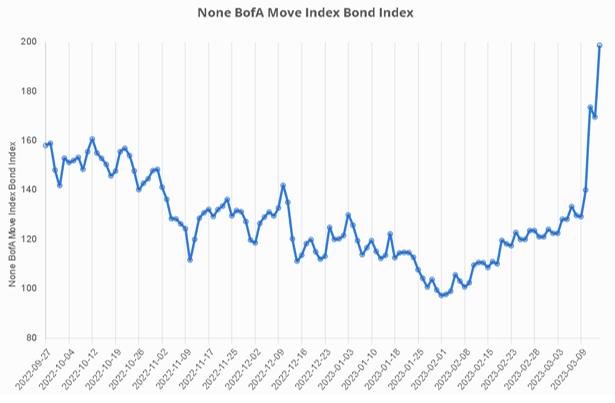

MOVE is the Merrill Option Volatility Index that is a measure of market expectations for future volatility and this declining trend is a positive for ACMBS products supporting risk and credit spread tightening.

Fed Minutes Disappoint

Rate cut expectations and stocks buoyancy both subsided Wednesday as minutes of the May meeting identified Fed concerns about persistent inflation and the timing of rate cuts. The previous month’s minutes singled out the sticky inflation numbers and that perception remains in place as sentiment for a rate cut has been reduced to one later this year.

Not Everyone is Cutting Rates

After eight years of negative interest rates the Bank of Japan is withdrawing its support of bond purchases as its ten-year Note now yields 1%, its highest rate since 2013 and after it was as low as -0.30% as recently as four years ago.

This tighter policy is directed at support for the Yen which had slid to its weakest level in 34-years.

The Week Ahead

More Fespeak, an active Treasury calendar, and Personal Consumption Expenditures on Friday.

Tuesday – Treasury sells $140 billion 13 and 26 week Bills, $69 billion 2-year Notes and $70 billion 5-year Notes.

Wednesday – Treasury sells $44 billion 7-year Notes and $28 billion 2-year FRN’s.

Thursday – 1QGDP expected at 1.6%.

Friday – Personal Income and Personal Consumption Expenditures.

May 20, 2024

Rally Continues

Weaker employment data coupled with lower than expected core CPI numbers have helped markets move up rate cut expectations to as soon as July. This stockscharts.com chart shows how the benchmark 10-year Note has returned to its 50-day Moving Average after having briefly touched its 200-day Average of 4.33% last Thursday.

As strong as this response has been equities have hit record levels with the DJIA closing above 40,000 for the first time in history, helped by a core CPI rate of 3.6% that was its lowest annual rate since April 2021, and following three months of stronger than expected numbers.

While not declining as fast as desired, Wednesday’s release at least suggests prices and economic activity are not reaccelerating, something a flat Retail Sales number helped to support.

It was a very active week for Fed officials led by Chairman Powell who stated that” by many meany, many measures” interest rates are high enough to slow demand as he repeated the Committee will have to see where the data fall out and people should not focus on one release but look at economic data in the aggregate.

One out of Three Not Enough

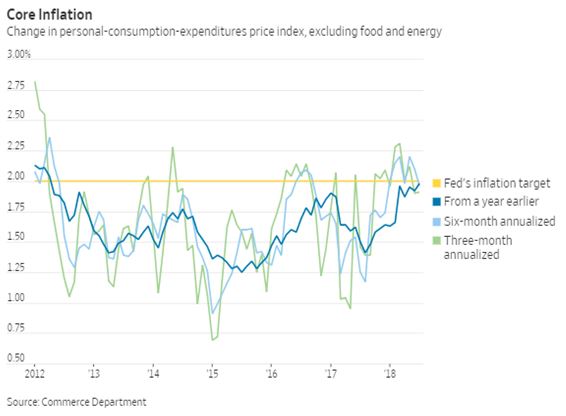

This chart shows how the main components of the Fed’s preferred inflation gauge have performed with the cost of housing and services still elevated with housing being the most stubborn. To get to 2% inflation the Fed does not need for each category to reach that level but housing at its current level of 5.6% in March does need to decline to the 3-3.5% area.

Mortgage rates that have been as high as 8% have been a deterrent to homebuyers so they have turned to renting and those rates have been slower to decline, possibly lengthening the time it takes to impact overall inflation.

The core PCE rate in March was 2.8% and the April report is scheduled for May 31.

The Week Ahead

Active Fedspeak continues, a light week for Treasury and economic reports.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Wednesday – Treasury sells $16 billion 20-year Bonds, Minutes of the May FOMC meeting are released.

Thursday – Treasury sells $16 billion 10-year TIPS, Jobless Claims and New Home Sales.

Friday – Durable Goods expected to be -0.5% and University of Michigan Consumer Sentiment.

May 13, 2024

Market conditions were favorable for the May 2024 504 debenture offering. Treasury yields had been on the rise between offerings from stronger economic data and consequent reduced chance of Fed rate cuts this year. The Friday before announcement, however, non-farm payroll gains were weaker than expected. On Thursday morning, before pricing, the CPI data came in as expected. Treasury coupon supply was not disruptive and there was no serious competing supply in our agency CMBS market.

Bank investors in the 504 offerings had been pretty scarce. especially after SVB and Signature Banks failed last March. Fed tightening led to sharply rising bank funding costs while more seasoned fixed rate assets in bank portfolios continued to pay low coupons. Some bank failures resulted as this negative carry punished banks. In recent months, however, banks have been repairing balance sheets while the Fed stopped tightening. As a result, more banks returned to the 504 debenture offerings. Banks took a substantial 44% of the May 25-year debenture pool.

Insurance buyers have been strong participants with the regular availability of higher 504 pool coupons, thanks to that rough bear cycle in interest rates. In the May offering, insurance buyers took a notable 40% of the 25-year pool.

That left spread-driven money managers to take just 16% of the 25-year pool this month. These buyers are critical to cover the deals when banks and insurance investors pull back. But they require a competitive spread to other products to be enticed to buy. As bank and insurance company buyers stepped up in the past six months, and benchmark comparable markets rallied in spread (agency MBS and agency CMBS), underwriters were able to place the 504 debenture pools at steadily tightener spreads to Treasury, from +115 bp in November to +75 bp in May for the 25-year maturity.

As we move toward summer, both the benchmark 504 debenture rate and spread have returned to right around 504 program lifetime averages as seen in the table below:

It’s fitting to return to program lifetime averages as Eagle changes guard in Selling Agents from me, Steve Van Order, to Glenn Doran starting in June. It has been my honor and pleasure to serve all of you in the 504 program for nearly 17 of the past 23 years, as I managed 199 debenture sales.

My successor, Glenn Doran, is a leading expert in federal agency finance. For many years Glenn ran all funding programs for the nationwide Federal Farm Credit Bank System, currently with $416 billion in debt outstanding. Glenn retired from Farm Credit at the end of April. Please join me in welcoming Glenn. Frank Keane, program Fiscal Agent since 2012, will continue to be your very expert and steady hand. Frank and Glenn will make a very strong team for years to come.

May 6, 2024

Fewer Jobs, Weaker Wage Growth

- 175,000 new jobs vs. a 240,000 forecast

- The unemployment rate rises to 3.9%

- Average hourly earnings rise just 0.2%, and decline to +3.9% y/y

- The benchmark ten-year rate drops 16 bps

- Stocks rallied to end the week higher, after having been weaker in previous sessions

- Traders increase expectations to two rate cuts this year

The markets recovered from a weak tone that had been set on Tuesday when the Employment Cost Index was higher than forecast at 1.2%, adding to inflationary pressures that the previous week’s PCE report had already established. At that point, ten-year Treasuries were higher by 38 bps on the month and the more policy sensitive two-year Note had reached 5%.

Supply

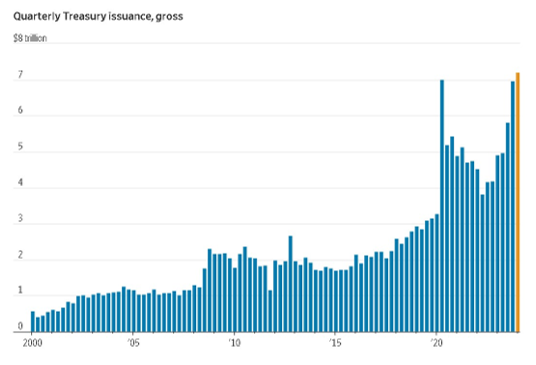

This stickier than expected inflation has amplified concern over the budget deficit and Treasury financing that is needed at a time when some auctions for longer dated maturities have seen reduced demand.

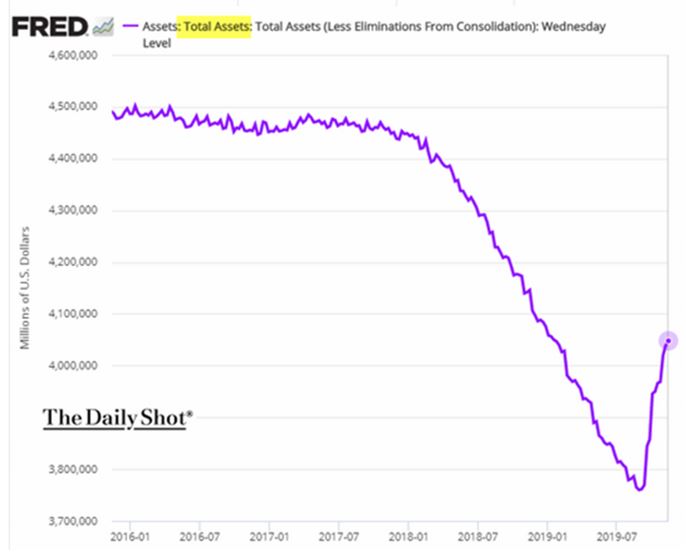

Some relief was provided Wednesday when Treasury announced plans to sell $1 trillion of bonds from May to July but said it would hold auction sizes steady. Additionally, they would cut by more than half the runoff from their balance sheet, to $25 billion per month from $60 billion.

As seen below the ten-year benchmark is 6 bps lower than when the 504 program priced its April debentures and this week’s sale will occur during the Treasury’s quarterly refunding for 3, 10 and 30 year auctions, but with a light ACMBS calendar.

FOMC

Resigned to fewer rate cuts than hoped for the FOMC meeting that concluded on Wednesday was as expected, no policy change but with a Jay Powell comment that soothed the market: “it’s unlikely the next policy move will be a hike.” As mild as that seems it did counter some analysts’ expectations that another 25 bps increase could happen.

Mr. Powell believes a soft landing for the economy is possible and though it is taking longer than thought there is a better balance of achieving the Committee’s employment and inflation goals. It is that balance that was supported by the jobs report that showed leisure and hospitality hiring slowed to 5,000 jobs in April from 53,000 in March. Coupled with food-service providers reports from Heinz and Starbucks showing increased caution among consumers Starbucks was as an outlier in Friday’s rally as its share price declined 15.9% on the week due to reduced demand in comparable store sales in the US and China.

The Week Ahead

Fedspeak resumes, the 504 program prices its May debentures, Treasury is active and few reports other than jobless claims.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – 504 program announces its May debenture sale, Treasury sells $58 billion 2-year Notes.

Wednesday – Treasury sells $42 billion 10-year Notes.

Thursday – 504 program prices its May debentures, Treasury sells $25 billion 30-year Bonds, Jobless Claims.

April 29, 2024

Tech Rebounds

A week that saw Treasury rates inch higher to 4.67% on the ten-year benchmark saw equities rally sharply after Microsoft and Alphabet beat estimates with their Thursday night releases. The Friday rally came despite another round of inflation data suggesting it remains higher than the Fed would like, yet it is not accelerating.

Close Enough

Personal Income was as forecast at 0.5% as was the monthly inflation rate of 0.3%, but the y/y rate of 2.7% was +0.2% above the February level, another reminder of how sticky inflation has become. Money markets are now pricing in only one rate cut this year, possibly as late as December, which is a big change from earlier this year when as many as six cuts were expected.

Orderly

It should not be a surprise that Treasury rates rose last week as the market absorbed $183 billion worth of Note auctions. Of the three maturities the $69 billion two-year Note was most in demand, attracting $182 billion in bids on Tuesday while demand for the seven year maturity on Thursday attracted the least amount of interest as investor demand for duration remains lighter.

Matching economic growth and inflation became a bit more confusing with Thursday’s release of 1.6% for the second estimate 1Q2024 GDP, far below the 4Q2023 rate of 3.4% and the previous estimate of 2.5% for the quarter. This slowdown as well as the recent inflation trend will be addressed on Wednesday as the FOMC announces its policy decision with Chairman Powell expected to confirm why recent data has forced the Committee to push back its timetable for rate reductions.

Other Reports

- High mortgage rates (7.45%) did little to affect New Home Sales for March that were above consensus at 693,000.

- Durable Goods was above consensus at 2.6% but February’s gain of 1.4% was reduced by half to 0.7%.

The Week Ahead

No Fed speak until Wednesday’s FOMC announcement, a light week for Treasury issuance, and Friday’s jobs report is the main data release.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – FOMC meeting begins, Consumer Confidence expected to decline.

Wednesday – FOMC announcement and Jay Powell press conference.

Thursday – Factory Orders expected to increase to 1.6%.

Friday – Non Farm Payroll expected to be 250,000.

April 22, 2024

Policy vs. Supply

As the second global conflict has passed its six-month mark in a seemingly choreographed fashion it is interesting to note not only what has happened, but what hasn’t happened, and that is a safe-haven trade in Treasuries. Since the October 7 attack by Hamas the benchmark ten-year Note has risen 75 bps as inflation has been described as sticky and sentiment has turned from expecting as many as six rate cuts this year to possibly one or two with some speculation the Fed may not cut at all.

Much of this recent shift can be traced to the April 10 CPI report of 0.4% that was above forecast and pushed this rate higher by 20 bps on the day and was followed by a weak auction for a thirty-year bond the next day. The Treasury announcement last Fall that it would emphasize debt issuance in the front end of the curve helped stabilize longer term rates and now that Fed officials and money market futures contracts identify just one or two cuts attention has turned to the supply of debt that will be needed to fund a deficit that is unlikely to decline in an election year cycle.

On a positive note, there could be some relief on inflation with this week’s PCE report that is expected to show its core rate unchanged at +0.3% with its y/y/ core rate declining to +2.7%.

Record Quarter

In the first quarter of this calendar year Treasury sold $7.2 trillion of debt, the largest quarterly total on record, and that builds on $23 trillion of debt sold last year. The Fed could aid absorption of this supply if it reduces its Balance Sheet runoff as it indicated at its March meeting. Currently, $60 billion of Treasuries and $35 billion in mortgage-backed securities mature each month and most officials favored reducing this amount by “roughly half.”

Unusual Situation

That is a description Chairman Powell used recently to describe how the economy has not become tighter in response to higher interest rates and an illustration of that is the 15% gain for the S&P 500 index dating back to the October 7 Hamas attack in Israel. That leaves stocks higher and Treasuries weaker at a time when neither move would have been expected.

Reports

It was a light week for reports, but they captured the conflict we face in analyzing activity. Retail Sales was +0.7%, stronger than the +0.4% forecast with February revised higher to +0.9% from +0.6%. Reflecting the current 7.5% thirty-year mortgage rate Housing Starts & Permits were 10% lower than forecast at 1.321 million.

The Week Ahead

Fed speak is reduced leading up to the April 30-May 1 FOMC meeting, an active week for Treasury, GDP estimate and the Fed’s preferred inflation gauge.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – Treasury sells $65 billion 42 day Bills and $69 billion 2-year Notes.

Wednesday – Durable Goods forecast at 2.8%, Treasury sells $70 billion 5-year Notes and $30 billion 2-year FRN’s.

Thursday – 1QGDP estimate revised to 2.2%, Treasury sells $44 billion 7-year Notes.

Friday – Personal Income forecast at 0.5% and core PCE 0.3% and 2.7%.

April 15, 2024

Last month we wrote the following: “This long bond bear fever has finally broken. Last week the Fed Chair stated the central bank was getting close to comfortable with starting to cut the target Fed funds rate. Markets expect a quarter-point cut in June. Actual and expected market volatility measure moderated thus far in 2024. “Risk-on” trading dominated and stocks hit new highs.”

That view was tested for this 504 offering. In April the Bond Bear came hungry out of hibernation. The March CPI inflation data disappointed and showed a mainly sideways trend in recent months, remaining stuck well above 3%. “Higher for longer” has returned with the futures market now pricing in only one or two quarter-point rate cuts from the Fed by year-end. Earlier in the year the market priced in up to six cuts. The ten-year T-note yield rose 48 bps from the March debenture pricing to 4.58%.

With the Fed finished with rate hikes, however, we recognize there has been a transition from a bear cycle to a bull cycle in its early stages. Painful bearish corrections like this are to be expected. What would change this view is if inflation trended stubbornly higher and the Fed had to reverse position on being finished with rate hikes and put them back on the table. That would be a rough ride. Market confidence in the nascent bull market was definitely shaken this month. The bull’s horns are quite nubby.

The April 25-year debenture rate, at 5.38%, was 41 bps above March and the highest rate since November of last year. The rate sat just 2 bps under the program life average of 5.40%. *The 25-year debenture rate spread over Treasury, however, continued to contract (7 bps m/m) and at T+80 bps was back to program life average. The recent bear cycle high for the spread was a half-point wider at T+130 bps in November 2022 and it was +115 bps as recently as last November. Despite the selloff in Treasuries, investors were in “buy the dip” mode which allowed for the spread tightening. This confidence to buy on dips in bond prices (e.g. on a rise in yields) comes from the belief the Fed tightening cycle is complete.

*We switched to using the 25-year maturity as the benchmark for rate and spread as of July 2019.

April 8, 2024

Slippage

Since the Fed has said its rate cut decisions will be data driven it is appropriate the market has slipped the last two weeks as it waited for end of week data like the previous week’s PCE that was disappointing.

Last week saw rates rise as market consensus embraced a slower path for the bank as it awaited Friday’s Non-Farm Payroll report, which was 303,000, far above its 208,000 forecast with the Unemployment rate declining to 3.8%, not traditional results for a tight monetary policy.

Market reaction saw stocks rally after a lackluster week while Treasuries continued to slip, closing the week at 4.41%. This weakness identifies the market’s concern that the Fed recognizes it has a sustainable economy and is more focused on controlling inflation and may be more patient than previously thought. That uninspiring performance for stocks ahead of the report also captures the mood of most people as a WSJ survey states: “What’s wrong with the economy? It’s you, not the data.” By significant margins respondents are negative on inflation, investment returns and the economy and though this is broad based it is interesting how much things have improved.

Acknowledgement of this strange economic twist can be found in comments by Chairman Powell last Wednesday when he said: “The economy isn’t becoming tighter, which it ordinarily would. It’s actually becoming a little looser, and you’re seeing inflation come down—very unusual situation.”

More data is forthcoming as CPI and PPI for March are released this week on the same days when Treasury will auction ten and thirty year maturities and the 504 program comes to market.

Higher

What is not unusual is that the market has moved to rates last seen in December as it questions whether a rate cut may happen as soon as June. At 4.41% we are 31 bps above where the 504 program priced its March debentures, but credit spreads are firm and secondary trade activity is brisk.

The Week Ahead

More Fed speak, the 504 program prices its April debentures, the quarterly Treasury refunding and inflation data.

Monday – Treasury sells $140 billion 13 & 26 week Bills.

Tuesday – 504 program announces its April sale, Treasury sells $65 billion 42 day Bills and $58 billion three year Notes.

Wednesday – CPI forecast at 0.3% and 3.7% y/y, Treasury sells $39 billion ten-year Notes, Minutes of the March Fed meeting are released.

Thursday – PPI forecast at 0.3% and 504 program prices its 20 & 25 year debentures.

Friday – Consumer Confidence expected to decline.

April 1, 2024

Sideways

The market moved sideways waiting for Friday’s PCE report and while markets were closed in observance of Good Friday the numbers came in as expected, leaving markets close to unchanged on the holiday shortened week.

The PCE price index excluding food & energy increased 2.8% on a 12-month basis and was up 0.3% from January.

Consumer spending increased 0.8% on the month, higher than the 0.5% estimate while personal income at 0.3% was softer than its 0.4% forecast.

Following this release in prepared remarks Chairman Powell repeated three quarter point interest rate reductions are planned while admitting “our position is we don’t know if progress on inflation will slow for more than two months.”

While the markets were stable, headlines were made by Fed Governor Christopher Waller who emphasized that strength has removed any urgency to cut rates, saying there is “no rush” to cut interest rates and the bank should push back the timing of cutting rates from their 23-year high. Waller also noted that the number of policy makers backing fewer than three cuts this year has risen. Lingering signs of strength can be found in recent increases in gas prices compounded by supply chain disruptions in the Middle East and now in the Baltimore port.

Reports

- Durable Goods orders were up 1.4% partially offsetting January’s level of -6.2%.

- New Home Sales were lower than forecast at 662,000.

- 3rd estimate of 4QGDP was 3.3%.

The Week Ahead

A heavy calendar for Fed speak with light Treasury supply and few reports, but with Employment data on Friday.

Monday – Treasury sells $140 billion 13 & 26-week Bills, ISM Manufacturing report.

Tuesday – Treasury sells $65 billion 42-day Bills, Factory Orders forecast at -3.6%.

Wednesday – Jay Powell speaks.

Thursday – Jobless Claims.

Friday – Non Farm Payroll expected to be 275,00, Unemployment 3.9% and Wages +4.1% y/y

March 25, 2024

Bumpy Road

Last week’s FOMC meeting was as expected with no change in policy as the Fed affirmed its plan for three quarter point rate reductions this year as the Committee expects “price pressure will continue to ease, and our policy rate is likely at its peak for this tightening cycle.” In his press conference Chairman Jay Powell admitted the path to lower inflation has been a bumpy road but the last two months don’t change the overall story.

That last two months’ comment refers to the recent inflation reports that were above forecast, pushing rates higher yet also sending stocks to record high closes.

Overall, markets are supportive of the central bank’s patient policy but there are pessimists who question why the Fed is announcing plans to cut rates when recent trends don’t support it.

This Financial Times chart is part of a story about an economist, Torsten Slok, who questions just that as the fed’s preferred inflation gauge is tracking higher over the last three months.

Slok believes that the Fed’s dovish pivot in December has created a strong tailwind for consumer markets, financial markets, and capital markets and this is causing inflation to reaccelerate and keep rates higher for longer.

Additional skepticism of rate cuts continues to come from former Treasury Secretary Larry Summers who believes the Fed has “itchy fingers” and needs to be more patient even as the Committee slightly increased its appropriate rate policy for 2025 to 3.6% to 3.9% and for 2026 to 2.9% to 3.1%.

This three-month chart of the daily close for the ten-year benchmark captures its rate dating from the “dovish pivot” in December to where we are today, slightly below its 4.33% range high and lower by 10 bps on the week.

Reports

Last week was light on reports focusing instead on the FOMC meeting, but this week provides the Fed’s preferred inflation report, Personal Consumption Expenditures and that is not expected to be lower.

The Week Ahead

More Fed speak with Chairman Powell speaking Friday, Treasury has an active week, and we get GDP and PCE updates.

Monday – Treasury sells $143 billion 13 & 26 week Bills and $66 billion 2-year Notes.

Tuesday – Treasury sells $67 billion 5-year Notes and Durable Goods expected to be +1%.

Wednesday – Treasury sells $43 billion 7-year Notes and $28 billion 2-year Floating Rate Notes.

Thursday – 2nd revision of 4QGDP expected to be 3.2%, Jobless Claims to be flat at 214K.

Friday – Personal Income expected lower at 0.4%, PCE forecast slightly higher at 0.4% and y/y at 2.5% with the yearly Core rate unchanged at 2.8%.

March 18, 2024

6 to 3

That is the change in the number of rate cuts the market expects now that inflation remains stubbornly high, and it is in sync with FOMC expectations. Markets now put the chance of an interest rate cut by June at just one in three vs. a 100% probability last month.

This alignment of thought pushed the ten-year rate higher by 22 bps on the week and the move started with strong CPI data that was later enhanced by the PPI Final Demand report on Thursday, plus a poorly received 30-year bond auction.

This news also impacted equities as the S&P 500 index suffered consecutive weekly losses for the first time since October.

Here is a table listing the monthly and annual numbers for the two reports and it was the PPI numbers that accelerated the rise in rates as inflation remains sticky amidst stronger than expected economic growth.

| CPI | PPI | ||||

|---|---|---|---|---|---|

| Prior | Consensus | Actual | Prior | Consensus | Actual |

With no change expected at the FOMC meeting this week analysts note it would take just two members to switch to two rate cuts this year and move the Committee’s dot plot higher. Such a move could also put at risk the number of rate cuts in 2025.

This stockcharts.com chart shows the ten-year Note’s four-month journey from 5% when “higher for longer” was in vogue to as low as 3.8% last month only to resume its rise after a second month of disappointing inflation data.

The Fed has indicated it is prepared to cut rates just not yet, so bond bulls need more patience as the data dependent central bank looks to avoid any stop/start approach to monetary policy especially as Treasury supply is expected to increase by $1.7 trillion this year. This amount is lower than last year but more weighted to longer term bonds which are riskier for investors and more difficult for the market to distribute.

Other Reports

- After declining by 0.8% in January Retail Sales increased by a less than expected 0.6% in February.

- Jobless claims were slightly weaker than expected.

- The University of Michigan Consumer sentiment survey declined as consumers appear to be in a holding pattern.

The Week Ahead

No Fed speak until the FOMC announcement on Wednesday, a light week for reports and Treasury has an assortment of maturities including the less than popular 20-year bond.

Monday – Treasury sells $146 billion 13 & 26-week Bills.

Tuesday – FOMC meeting begins, Treasury sells $46 billion 52-week Bills and $13 billion 20-year Bonds.

Wednesday – FOMC announcement and Chairman Powell press conference.

Thursday – Treasury sells $16 billion 10-year TIPS, Jobless claims, and Existing Home Sales.

March 11, 2024

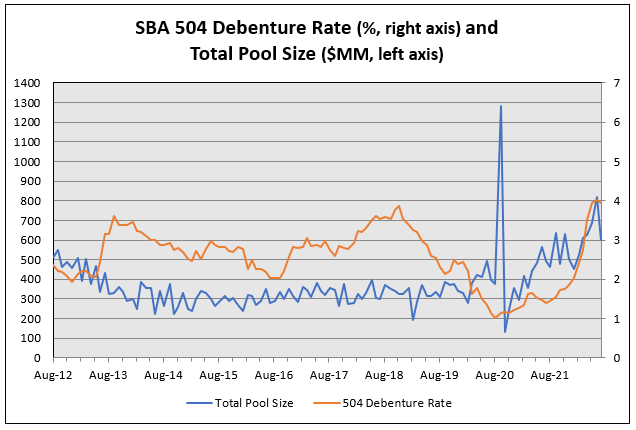

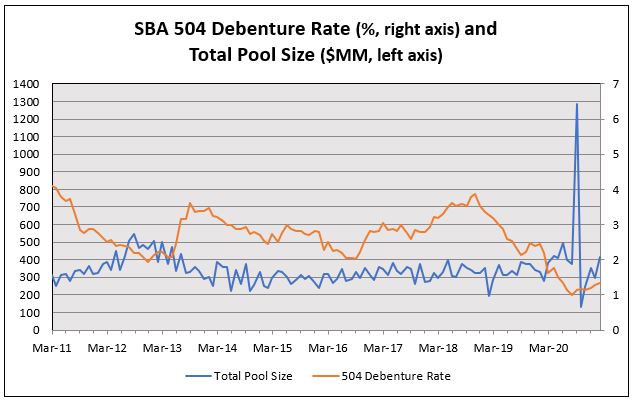

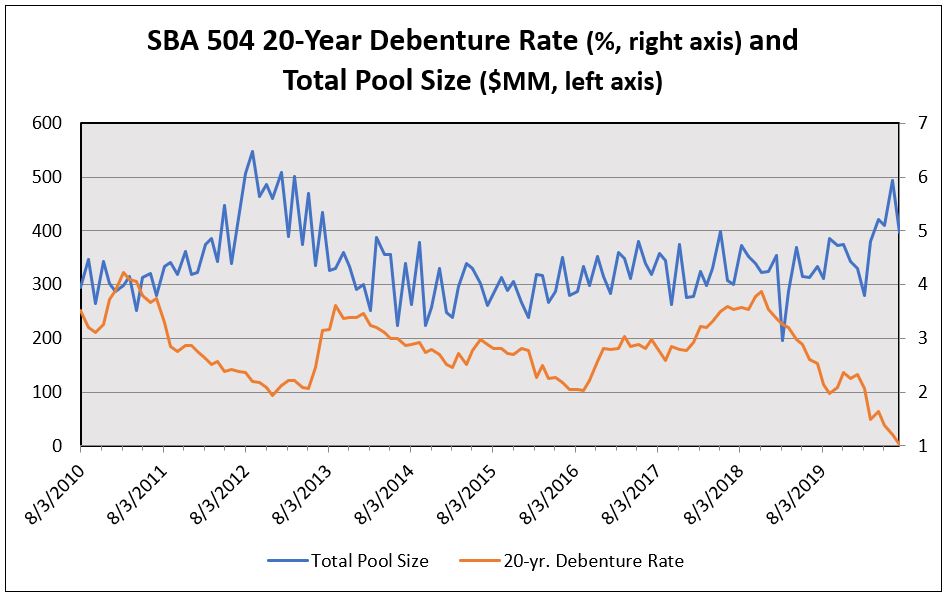

A calm market prevailed for the third-straight month for the March 2024 SBA 504 debenture offering. The benchmark 25-year rate ranged between 4.97% and 5.07% over the last three offerings. Sub-5% debenture rates for March were the first in nine months. Investor total demand has been very stable in 2024, at approximately $1.6 billion per offering. This excess demand over the amount offered allowed Eagle and Underwriters to tighten the debenture spread to Treasury from +113 bp in December to +87 bp in March, a reduction of 0.26 point. The benchmark 10-year Treasury yield fluctuated in a tight range of just 12 bp at the past three pricings.

The March benchmark debenture rate of 4.97% was 43 bp below the life of program mean. This past bear market cycle high was 5.82% in October 2023. The spread to Treasury of 87 bp was only 7 bp above life of program mean. This past bear market cycle wide was +130 bp in November 2022.

This long bond bear fever has finally broken. Last week the Fed Chair stated the central bank was getting close to comfortable with starting to cut the target Fed funds rate. Markets expect a quarter-point cut in June. Actual and expected market volatility measure moderated thus far in 2024. “Risk-on” trading dominated and stocks hit new highs.

Here’s hoping the period of calm lasts at least well into the summer. The markets have done a good job of ignoring geopolitical and domestic political risk, a testament to the powerful primary influence that US central bank decisions have over the markets. The political issue that poses the greatest risk to the bond market remains the debt ceiling, which is now firmly tied to debt default brinksmanship. Last year’s debt ceiling deal moved the issue to 2025, so that game will play out all over again post-election.

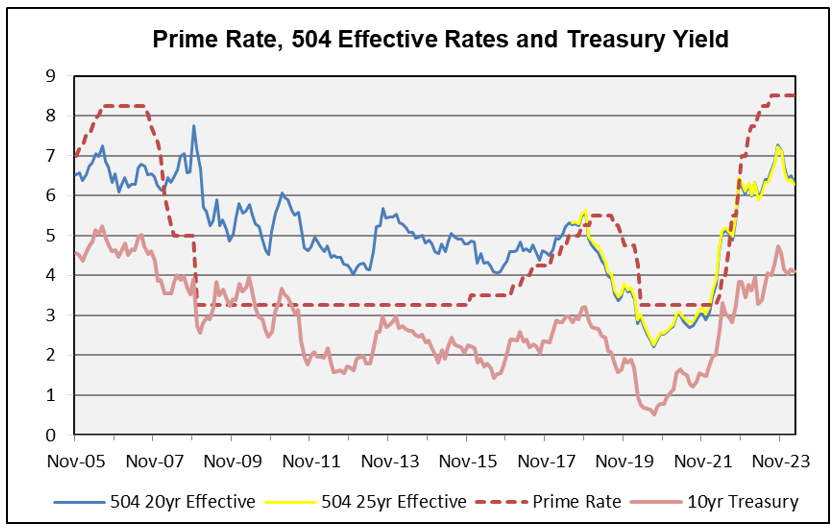

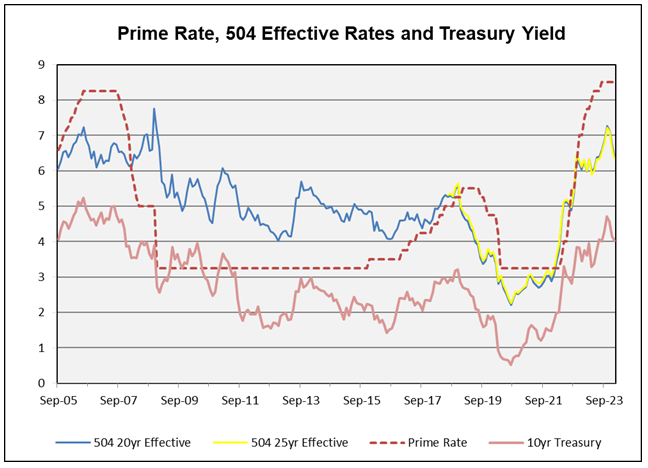

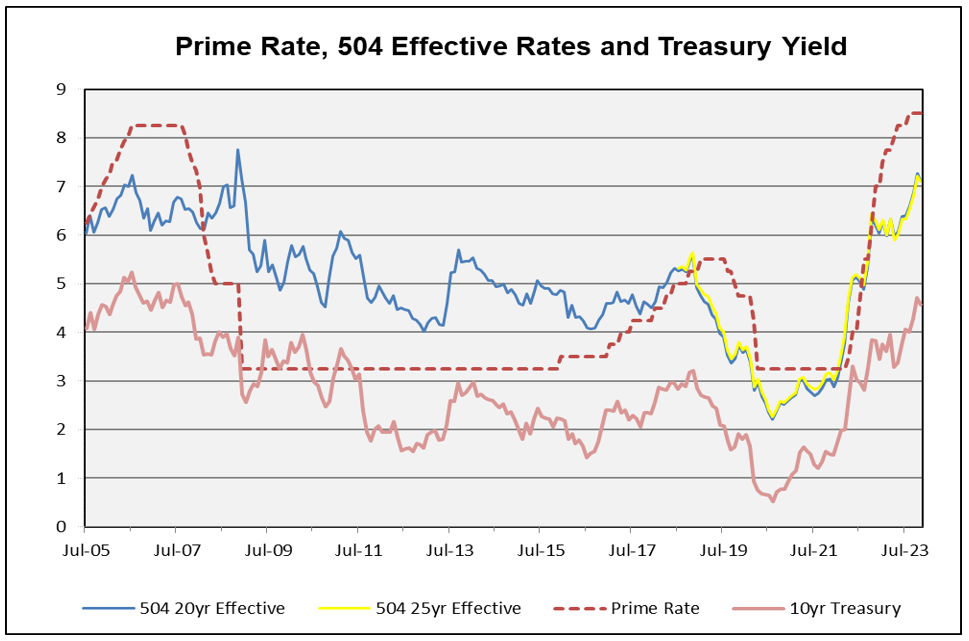

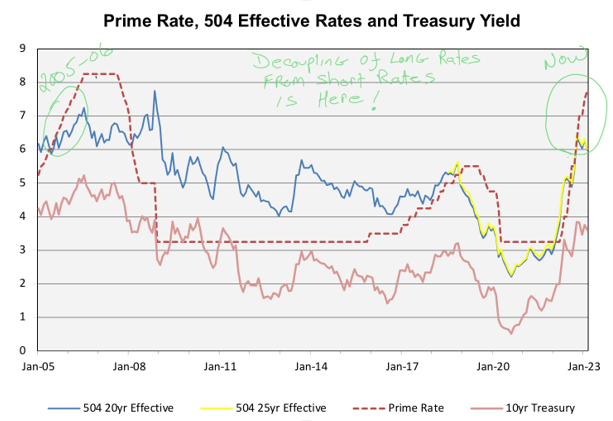

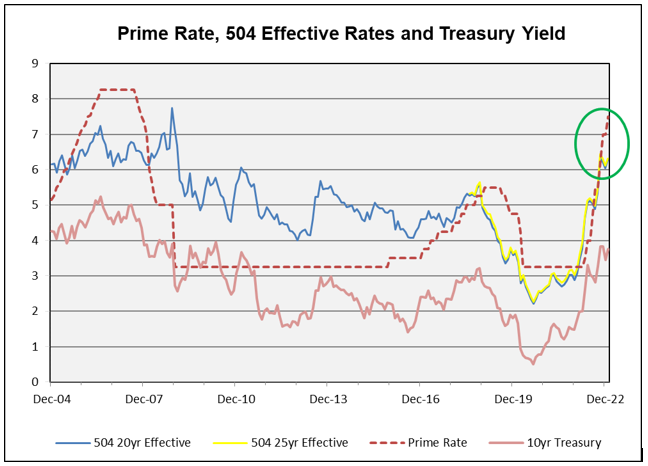

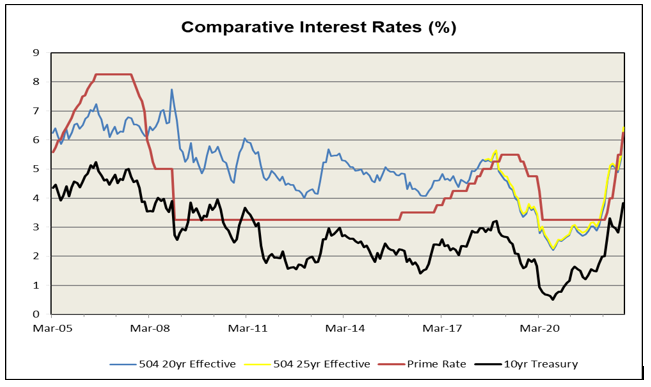

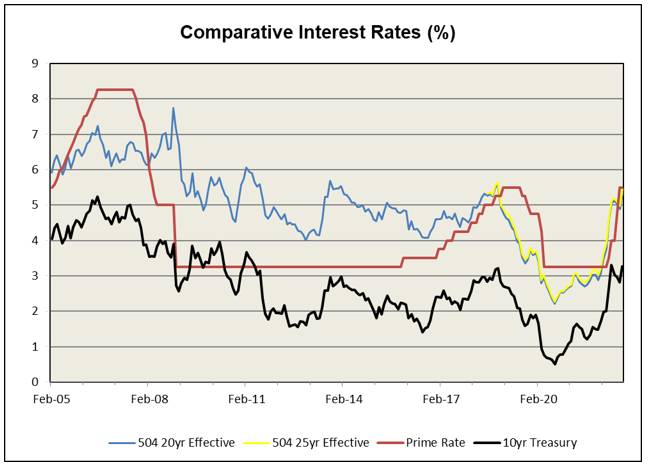

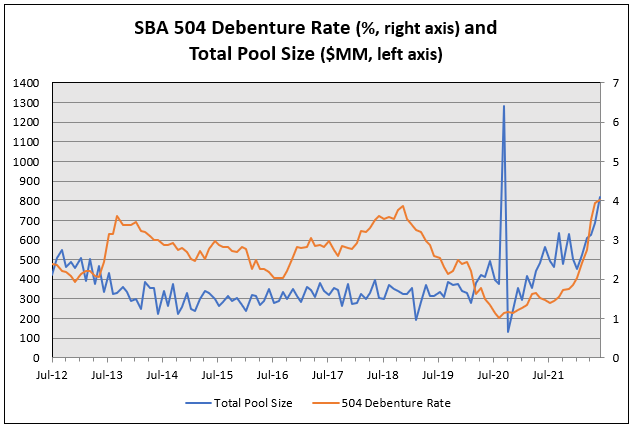

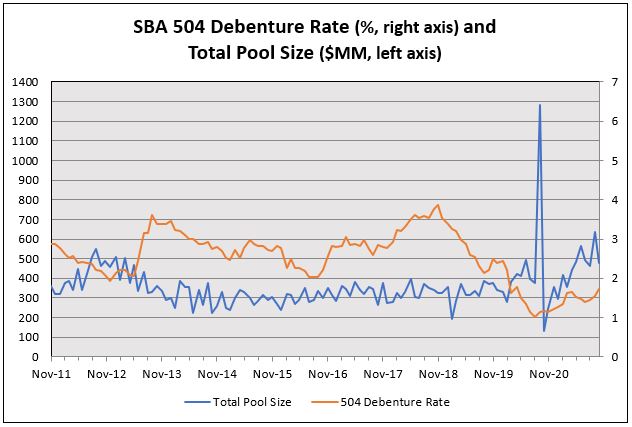

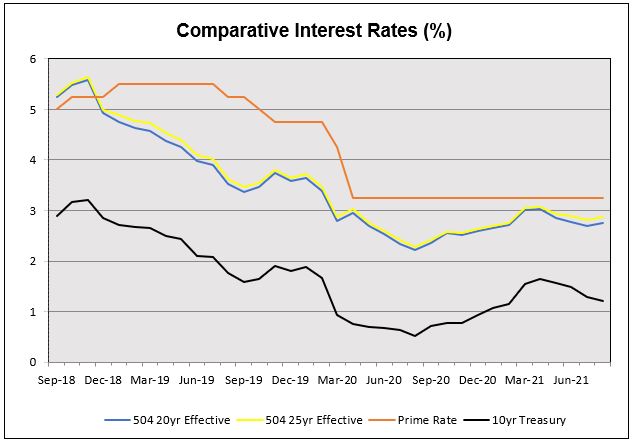

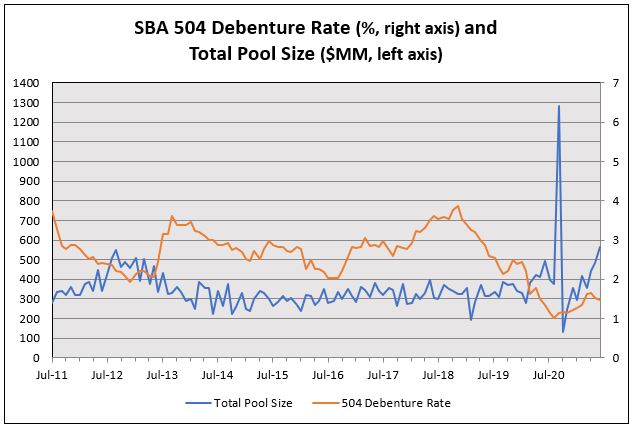

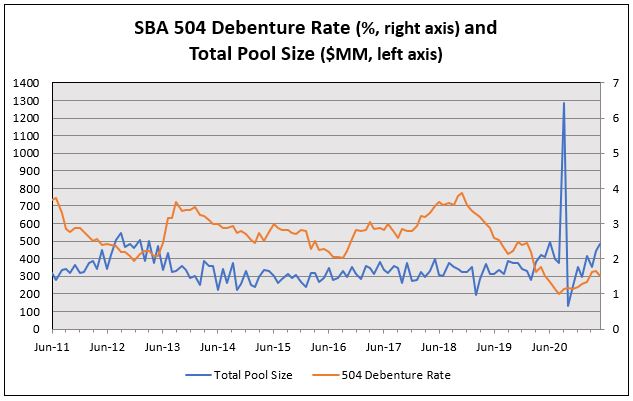

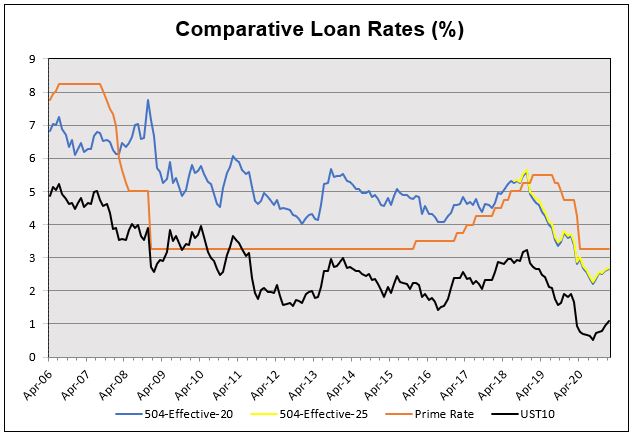

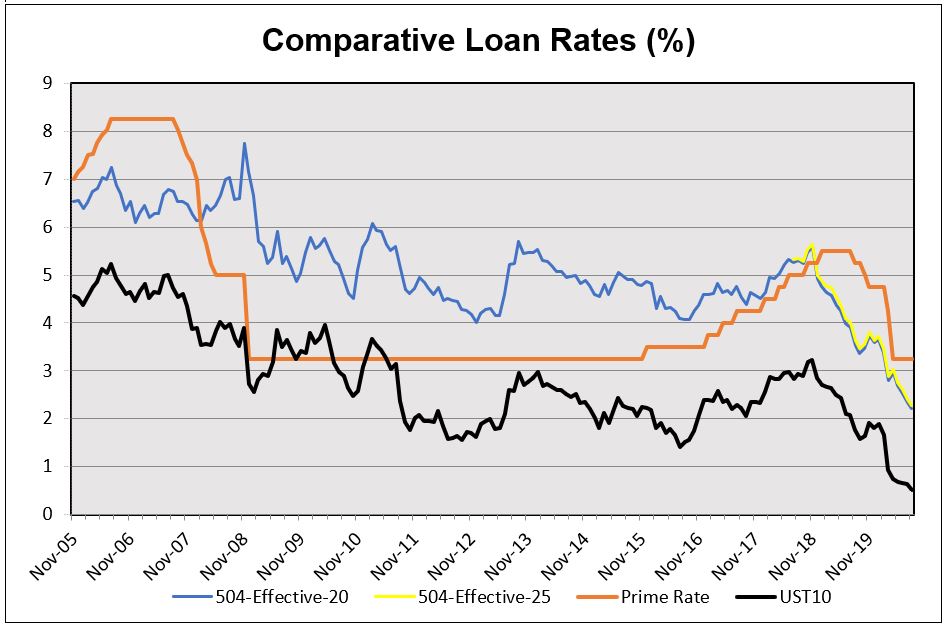

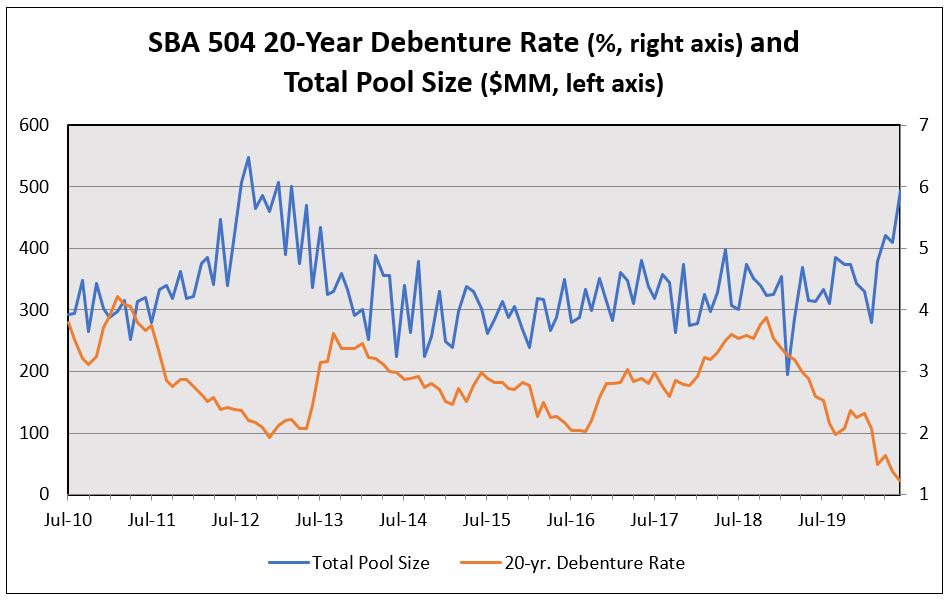

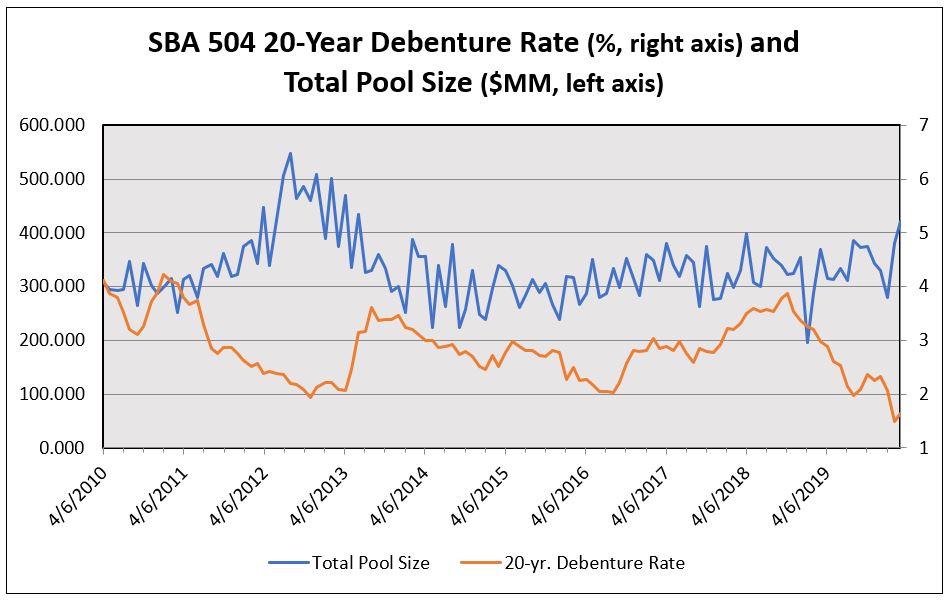

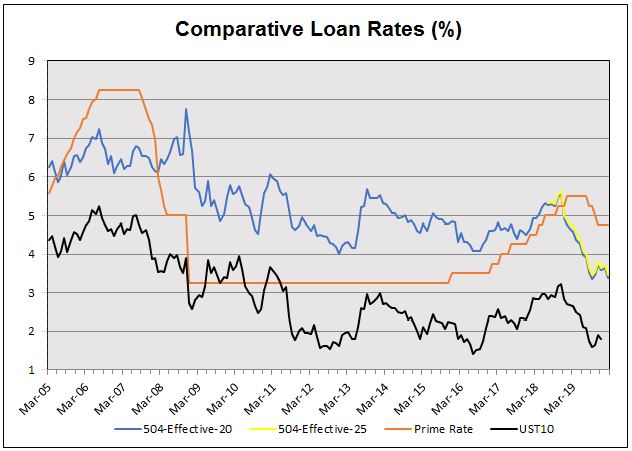

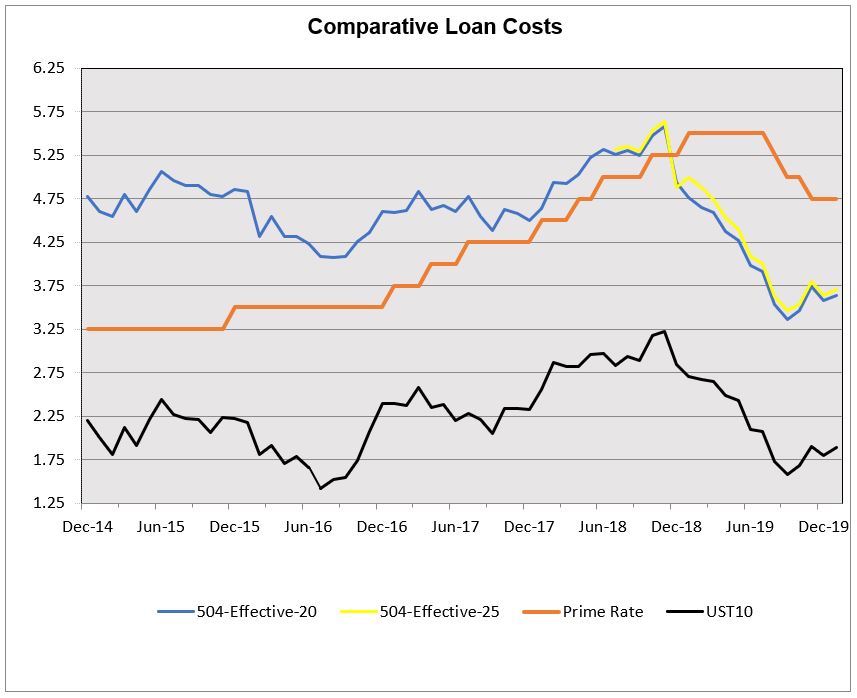

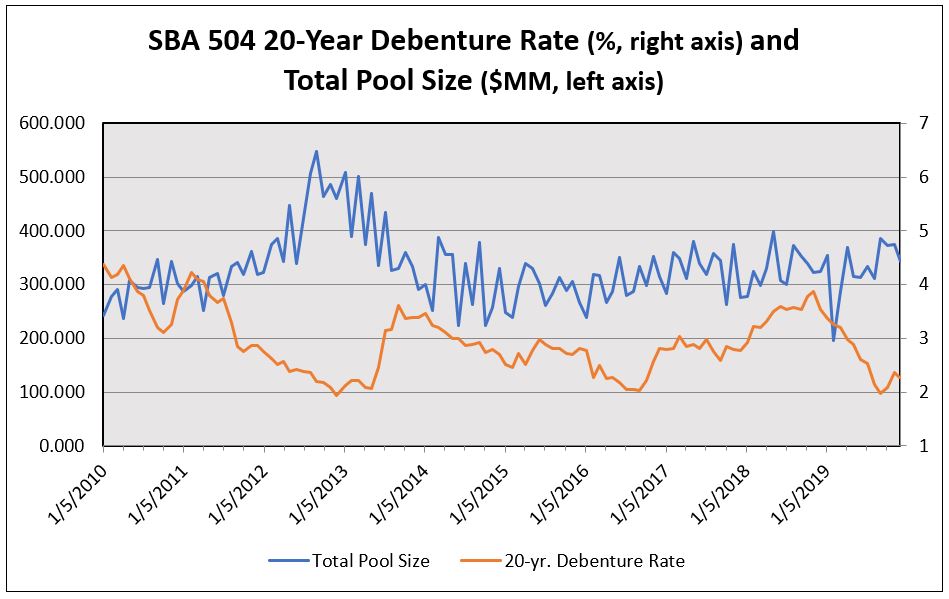

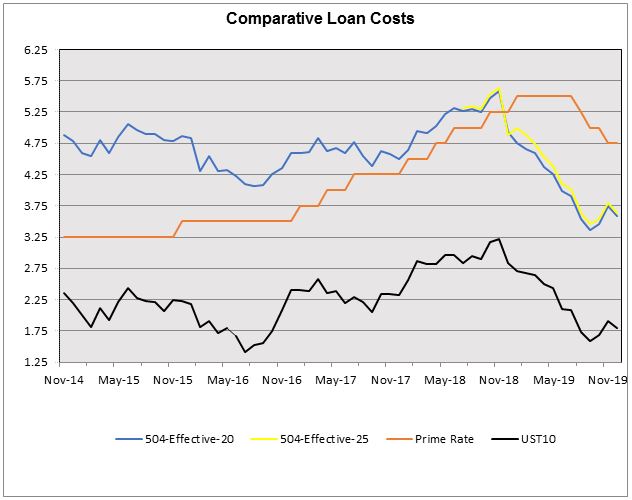

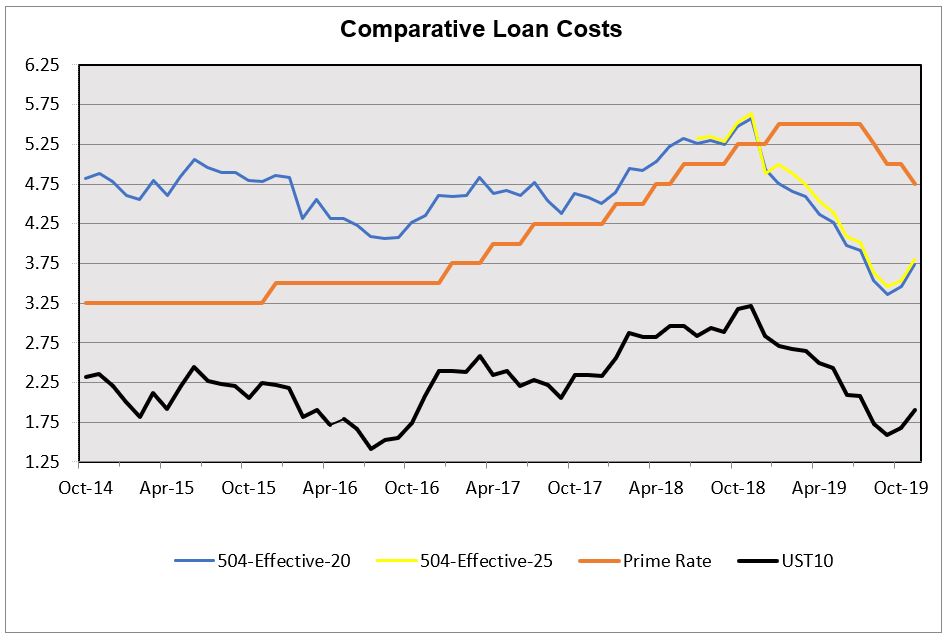

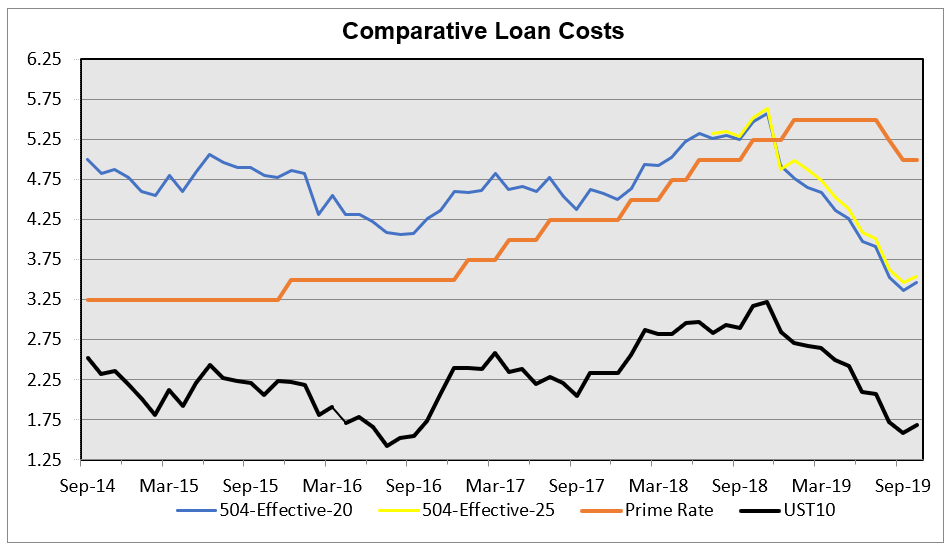

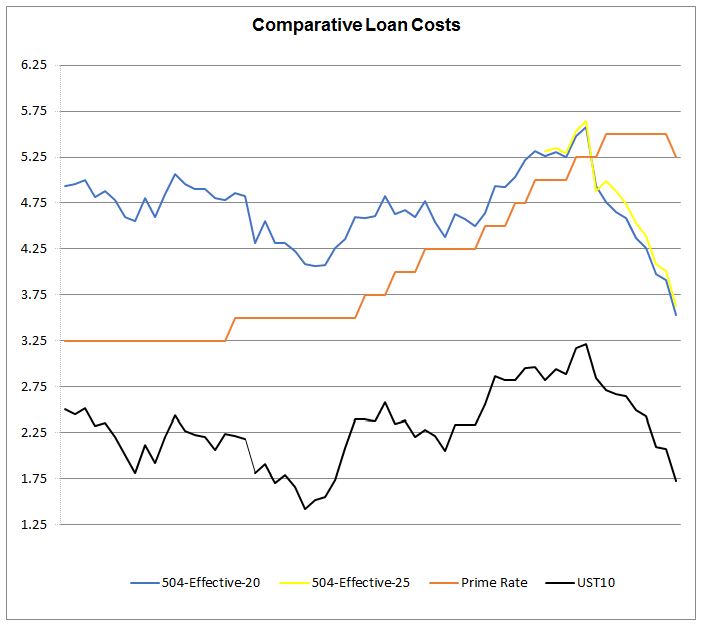

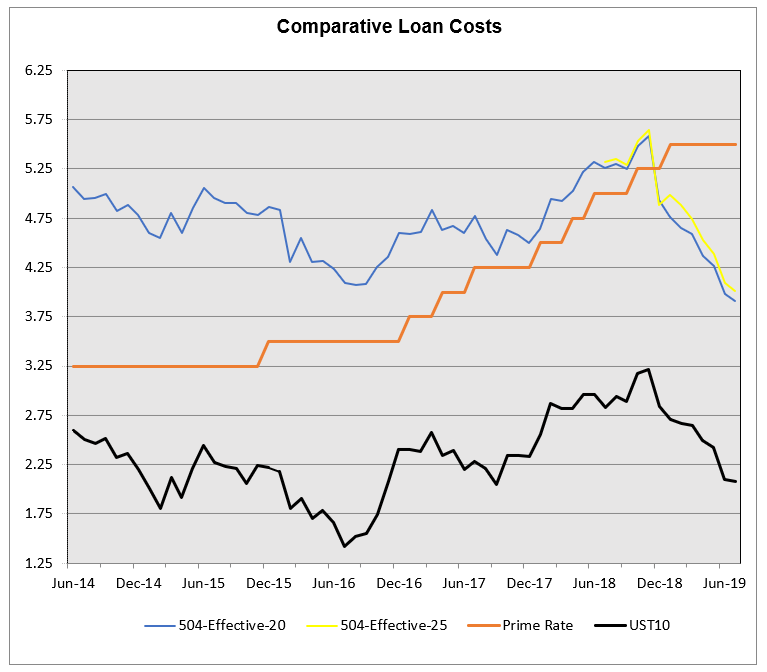

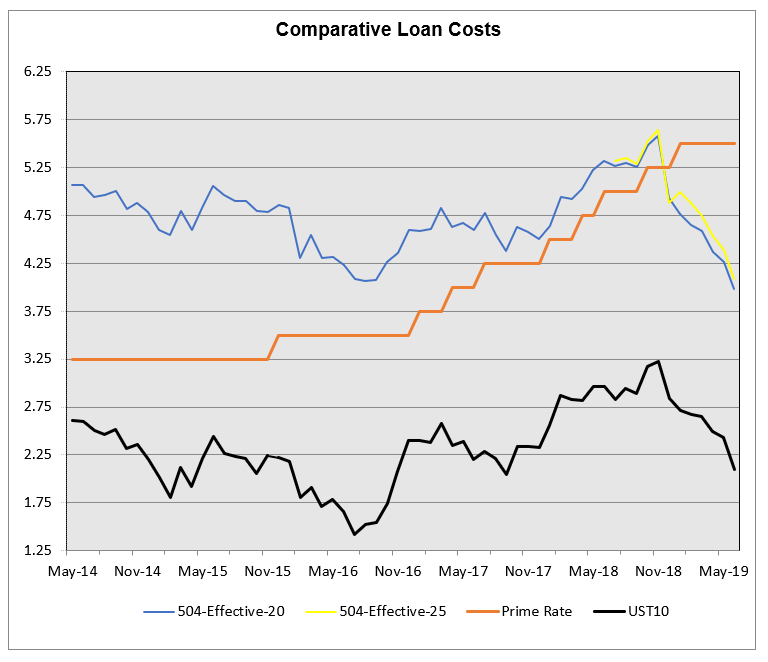

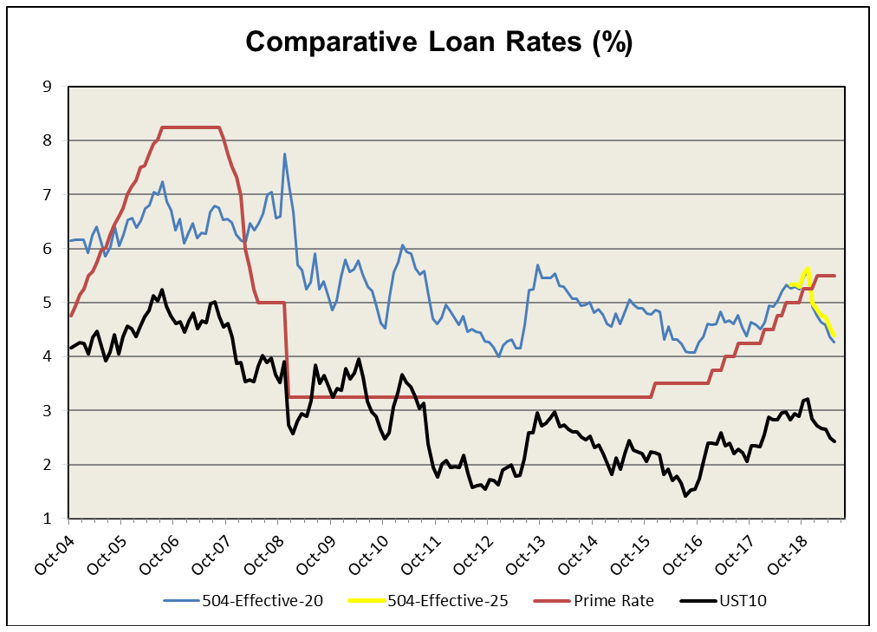

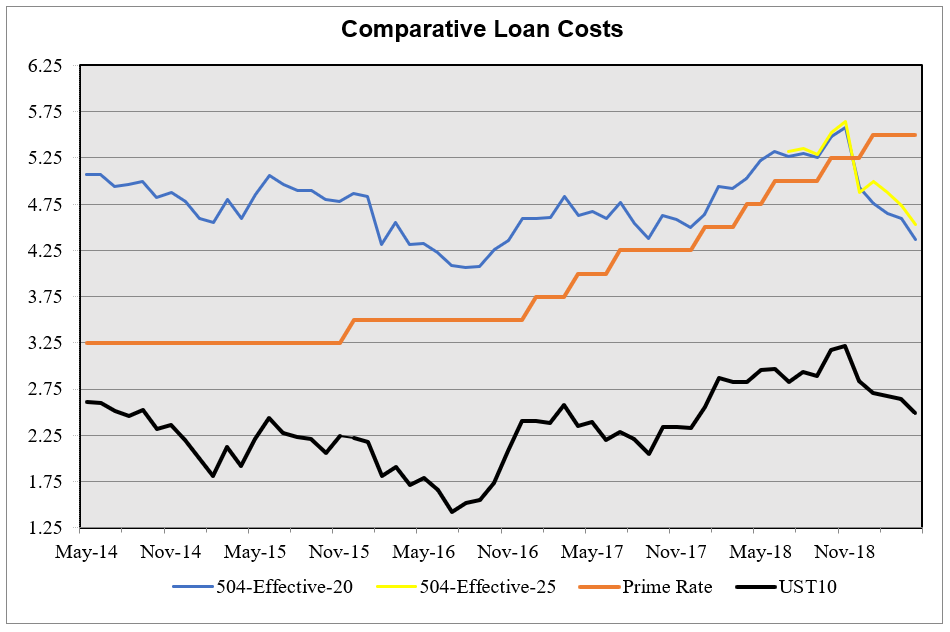

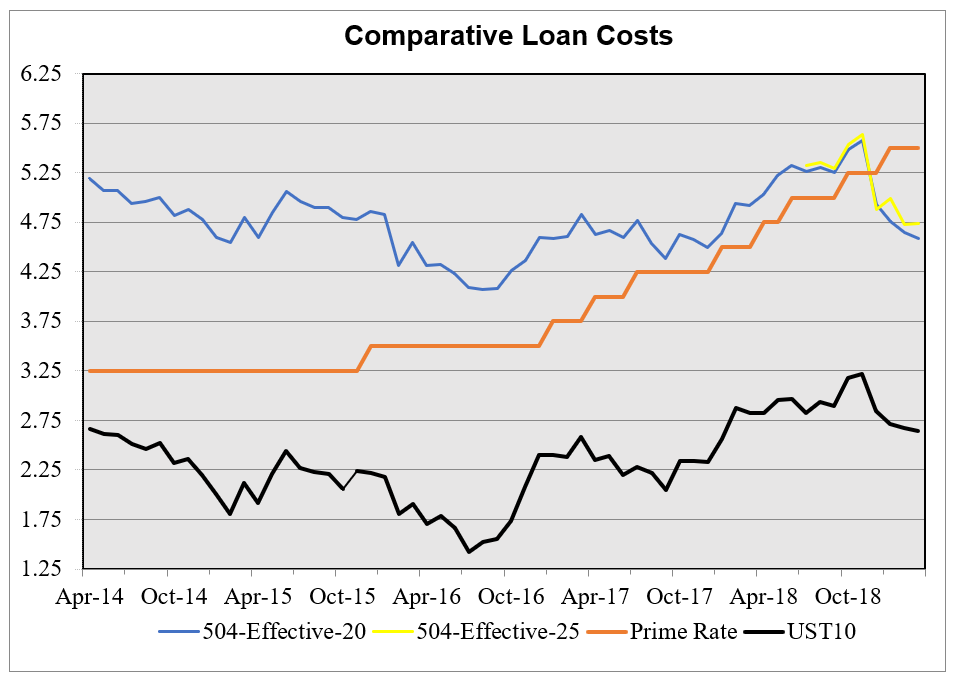

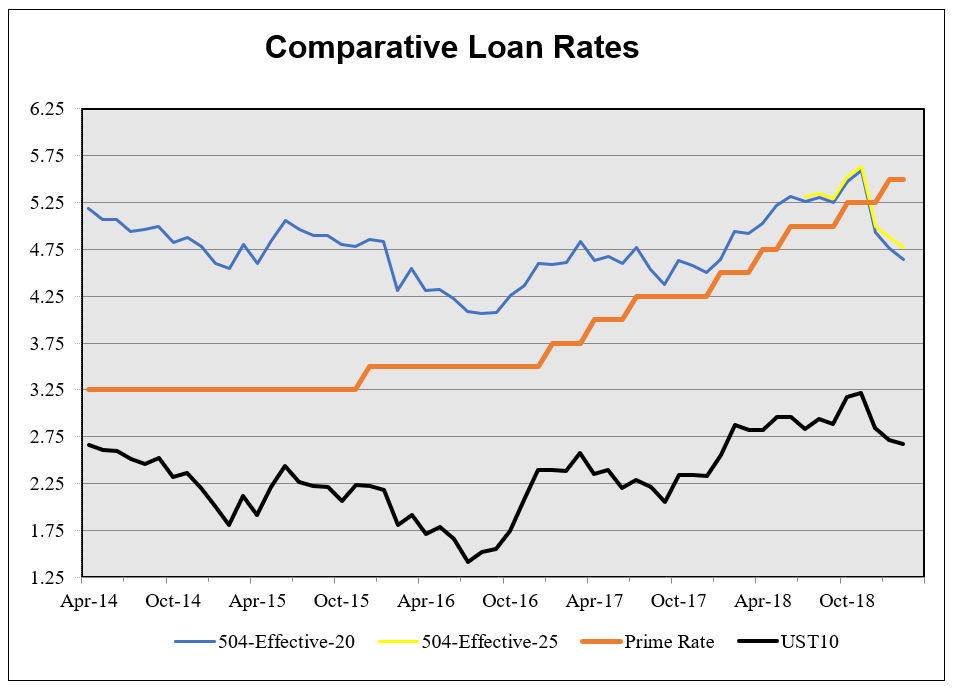

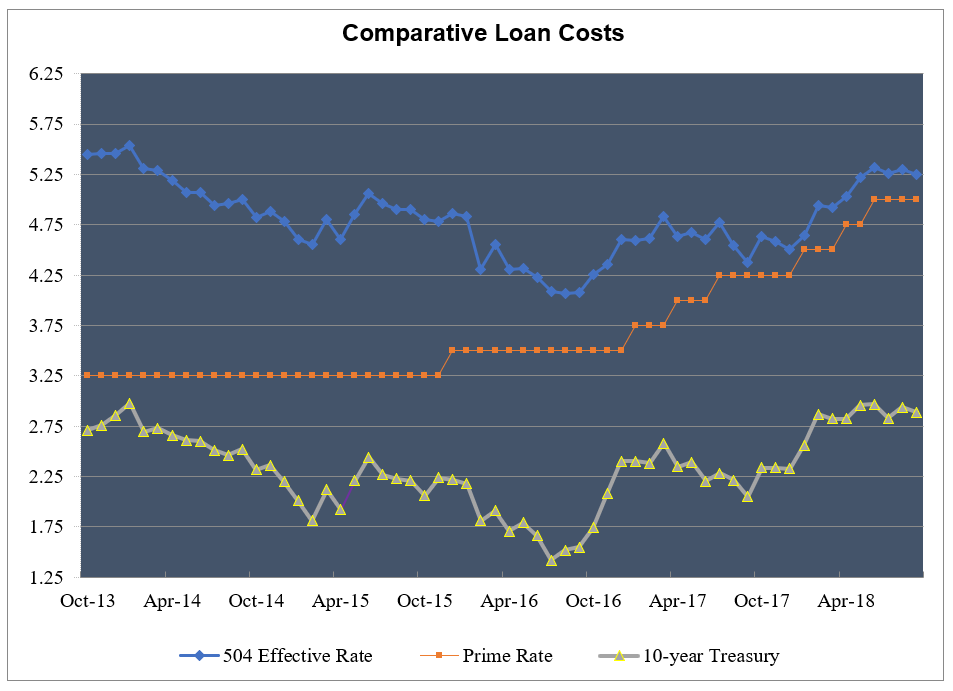

Our last comment is that for the remaining months the Fed funds rate is at a cycle high, there should be a cycle wide of the Prime Rate spread over the 25-year 504 effective rate. We can see this in the chart below, a chart Eagle posts on the website each month.

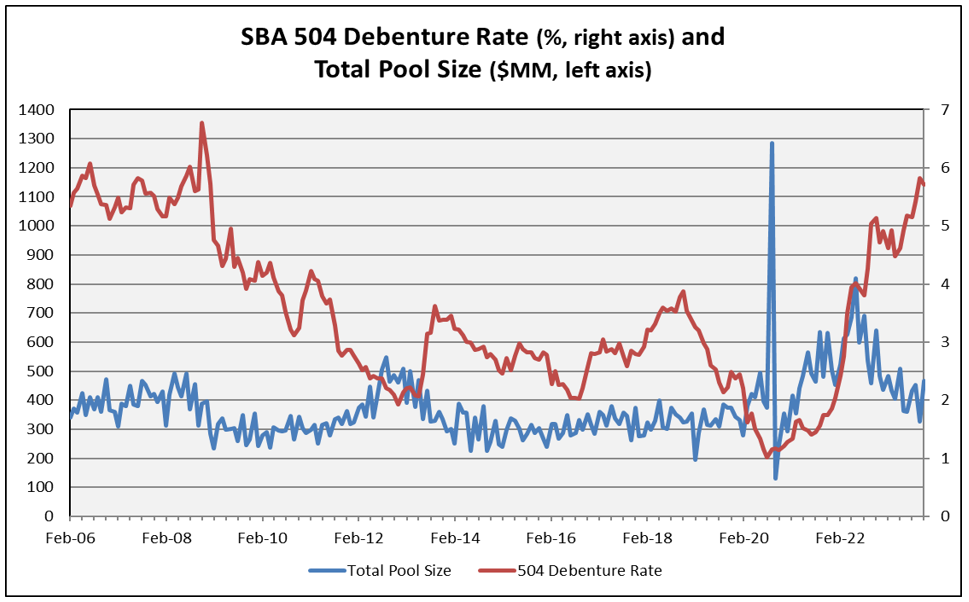

To put some numbers on it, this March the Prime Rate was 222 bp above the 25-year 504 effective rate. In the two prior Fed tightening cycles the Prime over 504 effective rate spread peaked at +179 bp in September 2019 and +216 bp in December 2006. *This month’s spread is in line with the 2006 experience that featured a Prime Rate of 8.25%, nearly identical to today’s 8.5% In 2019 the Prime Rate was much lower at 5.5%.

*The 504 effective rate was based on the 20-year debenture rate in 2006.

Inching Closer

It was a good week for inflation reports in the US and Europe with this Financial Times chart showing how the Fed’s current range of 5.25-5.50% has reduced CPI to 3.1% in January, down from a high of 9.1% in June 2022.

While this Financial Times chart refers to CPI it was last week’s PCE report that came in as forecast at 0.2% monthly and 2.4% y/y, with core readings of 0.4% and 2.6% y/y that fortified this improvement. These numbers remain above target, but the market is now resigned to slower and fewer rate cuts as the economy seems headed for a soft landing without an appreciable rise in unemployment, a feat few analysts expected.

One person who did believe in that is Fed Governor Christopher Waller whose philosophy was the usual jump in unemployment resulting from a tight monetary policy could be avoided if employers scrapped vacancies instead of laying off workers and it seems that is what happened since unemployment remains historically low at 3.7%.

Like this US trend Eurozone inflation declined 0.2% to 2.6% in February and while the ECB is not expected to cut rates at its meeting this week it is expected to give guidance for its first rate cut.

Rates

After rising midweek, the benchmark ten-year Note closed at 4.19%, possibly driven by a weaker than expected ISM Manufacturing Index report that was weaker than expected, leaving the Note 3 bps higher than when the SBA 504 program priced its February debentures.

Reports

In addition to the inflation data other reports were weaker than expected, a reminder of the Fed needs to balance its two objectives:

- New Home Sales were below consensus at 661K with 30 year mortgage rates at 7.06% vs. a recent low of 6.625% in December.

- Second revision of 4Q2023 GDP was 3.2%, .01 lower than its previous report.

- Durable Goods orders fell more than expected to -6.1%.

The Week Ahead

More Fed speak with Jay Powell before Congress, the 504 program prices its March debentures, a light week for Treasury, and the jobs report.

Monday – Treasury sells $149 billion 13 & 26 week Bills.

Tuesday – 504 program announces its March debenture sale, Treasury sells $80 billion 42-day Bills, Factory Orders forecast at -3.1%.

Wednesday – Jay Powell reports to Congress.

Thursday – 504 program prices its March debentures, Jay Powell reports to Congress.

Friday – Non-Farm Payroll expected to be 210,000 vs. the previous month’s 353,000.

February 26, 2024

Paused

The recent rise in rate took a break last week with the benchmark ten-year rate declining slightly to 4.26% as the 2/10 curve inverted further to -44 bps as hopes for a March rate cut have been dashed. This level is where it was last October before it rose to close near 5% on increased inflation fears. One difference between then and now, besides that same fear, is the Fed has convinced traders that an imminent cut in rate is not forthcoming and the number of cuts will be fewer than expected.

Wednesday’s release of the Minutes from the January 30-31 FOMC meeting underscored the Committee’s patience to be data dependent on any policy change with only two members highlighting the risks of keeping rates too high for too long. The Committee was wrong in 2021 when it believed inflation was transitory and does not want to ease prematurely only to be faced with a stop/start action should inflation rise again, and rates would need to be increased. Concern about inflation was evidenced by the comment that the Committee was “highly sensitive” to inflation risks and policy hawks could interpret that as the Fed being willing to raise rates should inflation persist. That is a view expressed by Larry Summers, a former Secretary of the Treasury, who believes there is a meaningful chance (15%) that the Fed could raise rates if they don’t see it trending lower. A Financial Times article notes that is the same odds of an NFL kicker missing a 37 yard field goal, but also the odds the New York Times gave of Donald Trump winning the 2016 election.

Reports

It was a very light week for reports but that changes this week as we get data on all the Fed’s topics of interest – the economy, inflation, and jobs.

- Economy – Wednesday’s release for second revision of 4QGDP is forecast at 3.3%. Durable Goods forecast is -0.5%, continuing the weakening trend in manufacturing.

- Inflation – Thursday is Personal Income and is expected to be 0.3% with Personal Consumption Expenditures forecast at 0.3% and 2.4% y/y with the core numbers slightly higher.

- Jobs – Jobless claims expected to be 206,000, consistent with recent weeks and following the larger than expected January jobs report.

The Week Ahead

Treasury issuance is active early in the week:

Monday – $149 billion 13 & 26 week Bills, $63 billion two-year Notes, and $64 billion five-year Notes, New Home Sales expected to be 680,000.

Tuesday – $42 billion seven-year Notes.

Wednesday – 4QGDP revision and Durable Goods report.

Thursday – Personal Income and PCE, Jobless Claims.

February 19, 2024

One, Two

After absorbing the first punch from CPI on Tuesday bond bulls took another hit on Friday when PPI also came in above expectations. Dovish sentiment weakened after the January 31 FOMC meeting and again after a Jay Powell interview on 60 Minutes that delayed rate cut expectations until June and reduced expectations to just 100 bps in 2024. An exclamation point for that sentiment is the admission the Committee will not even discuss rate cuts at its March 19-20 meeting.

Until that interview the market had continued to front-run the Fed in expectation of more rate cuts because:

- A hard landing for the economy was being discounted.

- PCE readings were moving in the right direction.

- Unemployment, while lingering near a historically low rate, was showing signs of increasing.

This benchmark Note had reached as low as 3.88% on February 1st and is now moving north of its 200-day Moving Average of 4.13%.

Reports

- Though the 0.3% monthly rate for CPI was not much higher than expected the 3.1% y/y reading, while lower than January’s 3.4% was above the forecast of 2.9%, triggering a spike in interest rates and a sharp decline in stocks where the DJIA had just recorded its fourteenth highest close this year.

- Retail Sales disappointed with a decline of 0.8% vs. December’s gain of 0.5% while vehicle sales represented a large portion of that drop at 0.6%.

- Industrial Production was expected to rise 0.2% but declined 0.1% and the Capacity Utilization Rate also was lower.

- PPI has consistently been lower than CPI as increases were not being passed along to consumers, but their nominal increases of 0.3% and 0.9% y/y were joined by their ex food and energy components of 0.5% and 2%, all above forecast.

Even with this softness the economy remains strong so it shouldn’t be a surprise that consumers may be taking a pause, but that could be the result of depleted pandemic savings and government support. Bank of America repots credit card and auto loan delinquencies are above pre pandemic levels with 30-year mortgage rates rising to 7.14% and those considerations could weigh on monetary policy should they continue.

So, the market waits for a June rate cut and the Fed stays true to its data dependency.

The Week Ahead

Fed speak continues; Treasury is active with a light week for economic reports.

Tuesday – Treasury sells $149 billion 13& 26 week Bills and $80 billion 40-day Bills.

Wednesday – Treasury sells $16 billion 20-year Bonds.

Thursday – Treasury sells $9 billion 30-year TIPS.

February 12, 2024

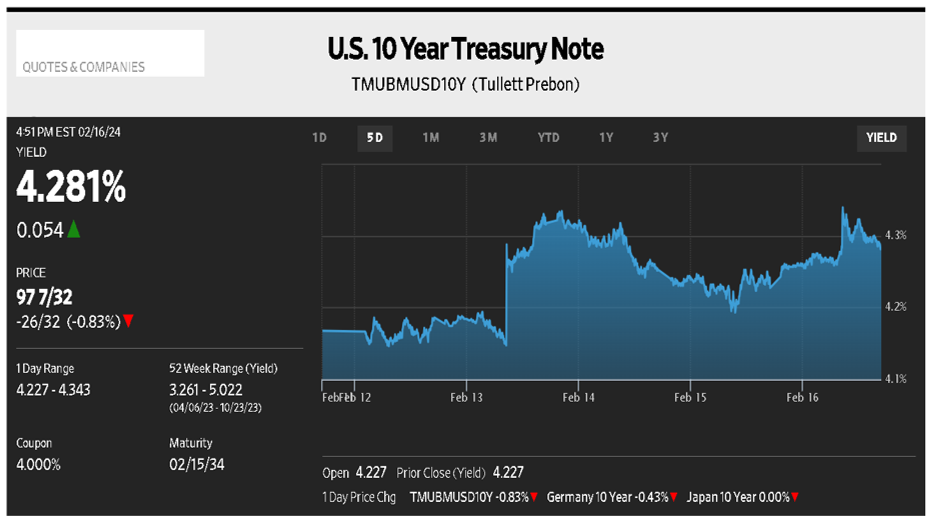

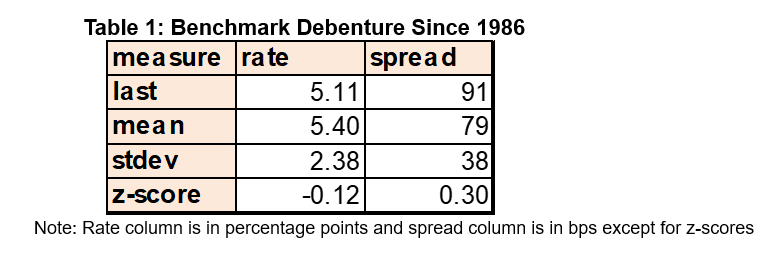

Another Strong Offering. The 504 debenture offering in February drew another round of strong investor demand, offering the opportunity to notably reduce spread over Treasury e.g., by 12 bps m/m for the 25-year pool. Strong anticipated and actual demand in recent months led Underwriters to recommend consistently tighter spreads to Treasury to the tune of a cumulative 24 bps tightening since the November offering. A strong bond market January Effect lingered into this offering, with investors flush with cash to put to work. Underwriters continued to draw from an expanded buyer base, 28 accounts participated in the 25-year offering, just one shy of the record 29 accounts in January.

Deal size helped results as well, with $315MM the smallest since January 2021. The 20-year pool size was under $13MM, the smallest since 1987, during the dawn of the 504 program. It seems there was a combination of calendar and seasonal effects behind the size. The processing window was a few days shorter than typical and, historically, there has been a bit of a seasonal effect regarding February producing smaller deal sizes. It’s reasonable to expect some rebound in March. Loan approval pipeline growth remains positive.

The 5.07% debenture rate for the benchmark 25-year pool was up 6 bps versus the prior offering and the spread was 12 bps tighter. This tightening of the spread offset much of the rise in the T-note benchmark yield.

Debenture Rates Nominal, Captain. Let’s put the current 25-year debenture rate and spread to Treasury in long-run historical perspective. The 504 program is in its 38th year and has been through many monetary policy cycles and crises of various magnitudes. Over the life of the program the rate for the benchmark 504 debenture maturity ranged from 1.01% (Aug. 2020) to 10.75% (Oct. 1987). The spread over Treasury for the 504 benchmark ranged from negative 4 bps (May 2021) to positive 349 bps (Dec. 2008).

February’s 504 benchmark rate of 5.07% and spread to Treasury of +91 bps were quite close to life of program means. We can measure that snugness looking at the z-score, or number of standard deviations from the mean, for the recent results. We display several measures, including the z-scores, in Table 1.

The debenture rate for February was 39 bps below the life of program mean with a z-score of -0.12 standard deviations. The spread to Treasury was 12 bps above the life of program mean with a z-score of +0.30 standard deviations. None of these measures are remarkable.

Free of The Bear, or Fooled Again? The market a year ago was in a similar situation to today. There’d been a rally in rates and spreads on expectation the Fed was nearly finished tightening and inflation was getting under control. The market front-ran the Fed, pricing in few or no more tightenings and a backing off of QT.

We know what happened, it was a very bad front-running call. Inflation moderated but the Fed kept hiking the Fed funds rate and kept up QT. Rates and spreads shot steadily higher from April through October. The market, in fact, twice failed to successfully front-run the Fed in this latest tightening cycle. The first bad call resulted in a selloff from August into November 2022.

As we discussed in December 2023 commentary, the bond market has again front-run the Fed. As a result, over the last several months, CDCs benefited from a sharp reduction in debenture rates, worth 71 bps for the 25-year maturity since October. Recently, however, the Fed and good economic data pushed back on the bulls. In just the past week the 10-year T-note yield rebounded off a retest of 3.80% up to 4.20%. That’s a sign the market is not yet fully out of the grip of bond bear.

There is good reason to hope the bond bear cycle is finally over. The Fed is forecasting a few rate cuts later this year. But the market yet persists in running too far in front of the Fed, leading to sharp corrections. It’s very pleasing debenture rates have declined so much in recent months, but we do caution that potential for high volatility still lurks.

*Stat-oriented folks may find it interesting that the median for rate and spread (5.32, +71) are pretty close to the mean, suggesting the distributions are not terribly skewed.

February 5, 2024

No Fed

The FOMC decision was to hold rates steady and indicate that any cuts were not imminent. A key phrase in the announcement was “the risks to achieving the inflation and employment goals are moving into better balance” and could lead to “adjustments” to the current target range of 5.25-5.50%. Chairman Powell stated that a rate cut in March was unlikely, putting more focus on May being the earliest that one could be expected.

The week began with rates finding support and declining into Wednesday when the FOMC announcement combined with the quarterly financing calendar for the Treasury and concerns over NY Community Bancorp’s stock declining 38% after a fourth quarter loss sent rates lower.

- Jay Powell took a March cut off the table and the market will now focus on May or June for the first of what is expected to be multiple rate cuts. Rates eased back once it was released and then resumed their move lower. The gains had accelerated earlier on Wednesday after the ADP jobs report came in at 107,000, significantly lower than its 145,000 forecast.

- Adding to that move was the Treasury’s announcement for its quarterly financing needs which will see the largest ever debt auctions with a maturity longer than two years. Of more interest was the caveat that if current projections are correct, they did not expect to increase auction sizes in future quarters.

- NY Community Bancorp cut its dividend after reporting a loss of $252 million after having purchased the assets of Signature Bank last year. This event, coupled with warnings from other banks about commercial loan losses, led the KFW Regional Bank Index to its worst day since the Silicon Bank collapse last March.

U-Turn

After extending its rally to a low of 3.82% the benchmark ten-year Note reversed course on Friday in response to the much stronger than expected jobs report showing a gain of 353,000 in January with an upward revision of 117,000 for December. Unemployment remained at 3.7% and the additional strength of 0.6% in average hourly wages (4.5% y/y) identifies how hot the economy is. This is one category the Fed will closely watch as it strives to balance employment and inflation.

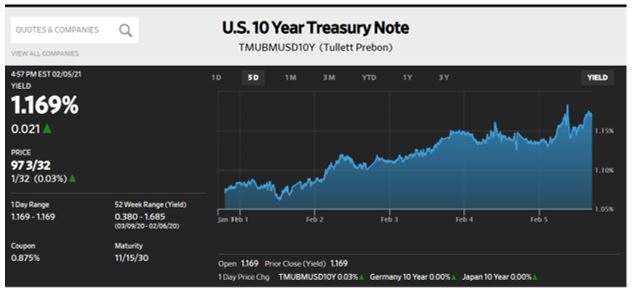

As seen in this WSJ chart the benchmark Note is basically unchanged from when the 504 program priced its January debentures.

Other News

- Like the Fed, the Bank of England left its key rate of 5.25% unchanged but signaled it is likely to reduce the rate sometime later this year.

- With borrowing costs expected to fall the International Monetary Funnd said the global economy is likely headed for a soft landing this year.

The Week Ahead

Fed speak resumes, SBA 504 program prices its February debentures, Treasury conducts its quarterly refunding, and a light week for reports.

Monday – Treasury sells $149 billion 13 & 26 week Bills.

Tuesday – 504 program announces its sale, Treasury sells $54 billion three year Notes.

Wednesday – Treasury sells $42 billion ten year Notes.

Thursday – 504 program prices its February debentures, Treasury sells $25 billion thirty year Bonds, Jobless Claims.

January 29, 2024

Support or Resistance?

With the ten-year benchmark closing at 4.14% Friday the question is – does it bounce back off that 50 day Moving Average or continue its move higher, above the 200 day average of 4.08%. In just three months, with market sentiment not Fed action driving its moves, we have seen the rate as high as 5% and as low as 3.88% as higher for longer gave way to expectations of as many as four rate cuts this year.

Supply

And now we prepare for Wednesday’s Treasury announcement of its upcoming quarterly refunding that can have a market impact based on where the supply is concentrated. Sensitive to demand for longer term debt, terms of the November refunding skewed towards shorter maturities and along with improving inflation data contributed to the year-end rally and partial normalization of the 2/10 Treasury curve.

With a stronger than expected 3.3% gain for 4Q GDP, coupled with a 2.6% y/y increase in the Fed’s preferred inflation gauge, Friday’s jobs report will be another item for the Fed to consider before making any policy change. Estimates for that release are 180,000 just like in December when the report was stronger than forecast at 216,000.

The market is expecting a rate cut at the March 19-20 FOMC meeting so the Committee will have two employment reports to analyze along with one more report on Personal Consumption Expenditures as it balances those numbers with an economy that has been surprisingly resilient.

The Week Ahead

Fed speak blackout until after this week’s FOMC concludes on Wednesday, a light week for Treasury and reports.

Monday – Treasury sells $149 billion 13 & 26 week Bills.

Tuesday – FOMC meeting begins.

Wednesday – FOMC meeting concludes followed by Jay Powell press conference. Treasury announces its quarterly refunding plans.

Thursday – Jobless claims forecast at 210,000.

Friday – Non-Farm payroll forecast at 180,000.

January 22, 2024

Fed Speak

That is what started the move higher in rates last week and there was a lot of it. There were as many as seven speeches given by Fed officials starting with Christoper Waller, a member of the Federal Reserve Board of Governors, who began the week by downplaying the need to rush to cut rates and subsequent speeches echoed that theme, driving the benchmark ten-year rate higher by 19 bps on the week.

That talk was joined by a poorly received 20-year bond auction and strong economic data as both Retail Sales and Industrial Production came in above forecast, like 4QGDP is expected to do when it is released tomorrow. Consensus is for a 2% increase that would put its annual rate at +2.8% from a year earlier.

This strength identifies the dilemma faced by the Fed as it prefers the market to be more cautious about rate cuts that might support economic expansion when it is not needed.

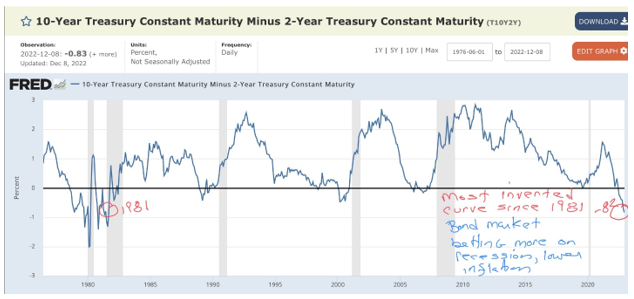

Recent Fed comments that more rate hikes are unlikely fall short of the central bank easing policy and the slope of the 2/10 cure reflects that uncertainty. It closed 2023 at -37 bps, moved to a more normalized level of -18 bps on January 12 and resumed more inversion at -26 bps last Friday. To be determined is how the curve will move, by short term rates declining due to rate cuts or by long term rates rising because rates will remain higher for longer.

Surge of Confidence

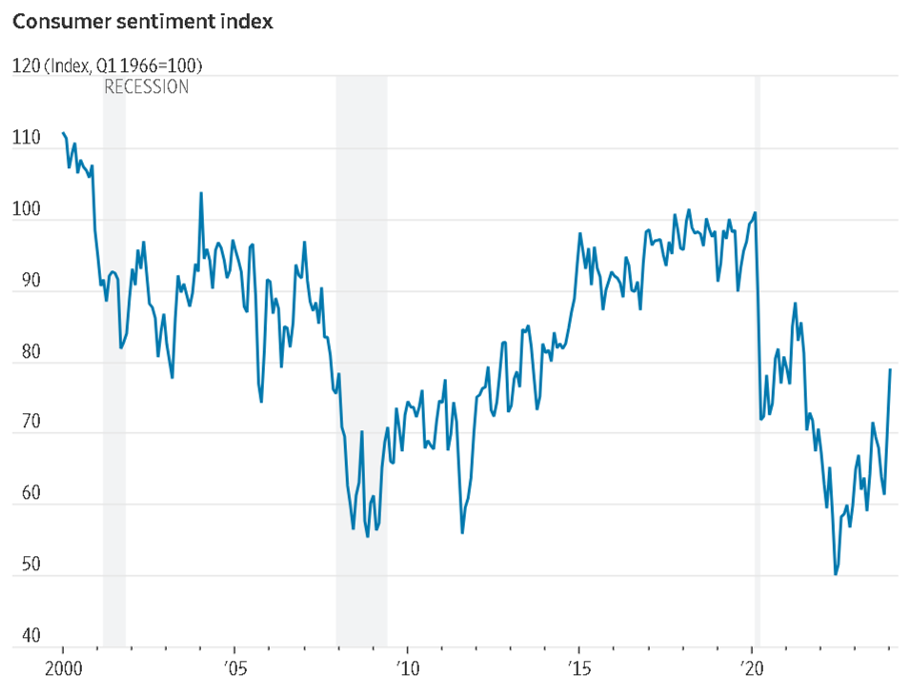

The University of Michigan Consumer Sentiment Index surged for the second consecutive month with a two-month increase of 29%, the largest two month gain since 1991.Reflecting the moderation of inflation, coupled with Fed comments that rate increases are behind us can lead to increased consumer spending and make the Fed more cautious about lowering interest rates.

The six month reading for the Fed’s preferred inflation gauge ended December at 2% and Friday’s release will be the week’s key report leading up to the January 30-31 FOMC meeting.

The Week Ahead

Reduced Fed speak leading up to the meeting, an active Treasury calendar and PCE on Friday. Continued elevated amounts of Investment Grade issuance can be expected as January has so far represented the largest amount of sales since 1990.

Monday – Treasury sells $147 billion 13 & 26 week Bills.

Tuesday – Treasury sells $46 billion 52 week Bills and $60 billion two-year Notes.

Wednesday – Treasury sells $61 billion five-year Notes and $28 billion two-year FRN’s.

Thursday – Treasury sells $46 billion seven year Notes. 4Q2023 GDP estimate, Durable Goods forecast at 1.5%.

Friday – Personal Income forecast at 0.3% and PCE expected to be flat and 2.6% y/y.

January 15, 2024

The 504 debenture offering in January drew strong demand for all three pools offering us the opportunity to reduce debenture rate spreads over Treasury and take advantage of a somewhat lower 10-year Treasury yield versus December. The 5.05% debenture rate for the benchmark 25-year pool declined 23 bps versus the prior offering and was the lowest in seven months.

Spurring the strong demand from investors was the belief, supported by Fed leadership, that the tightening cycle was complete. The market, as is typical, then front-ran the Fed, pricing in Fed funds rate cuts as early as the spring, a move is not supported by Fed guidance.

The market tried and failed a few times earlier in the tightening cycle to time the Fed and the result of the failures was not pretty as bond yields and spreads to Treasury quickly made new legs higher. The recent calming of key inflation rates and more neutral Fed speak, however, gives the market a longer leash, and has improved investor sentiment toward bonds quite dramatically. After the fast run in the 10-year T-note yield from 5% to 3.8% (before correcting up to 4% lately) it seems the market has more consolidation and/or correction ahead.

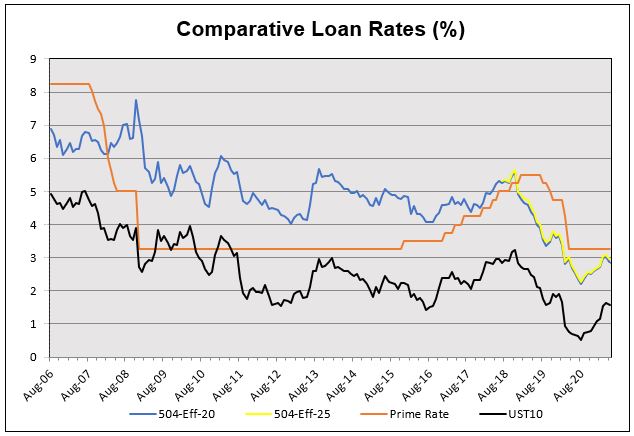

The chart below shows four key interest rates for the 504 program. We can see in recent months the sharp drop in 20- and 25-year 504 effective rates from around 7.25% in October to below 6.5% in January. The 504 effective rates for January were roughly 200 bps below the Prime Rate and that’s about as wide as it got at the end of prior tightening cycles. Looking ahead, based on Fed funds futures prices the market, in effect, very much expects the Prime Rate to be reduced along with the Fed funds target by a quarter point in March.

January 8, 2024

Slight Reversal

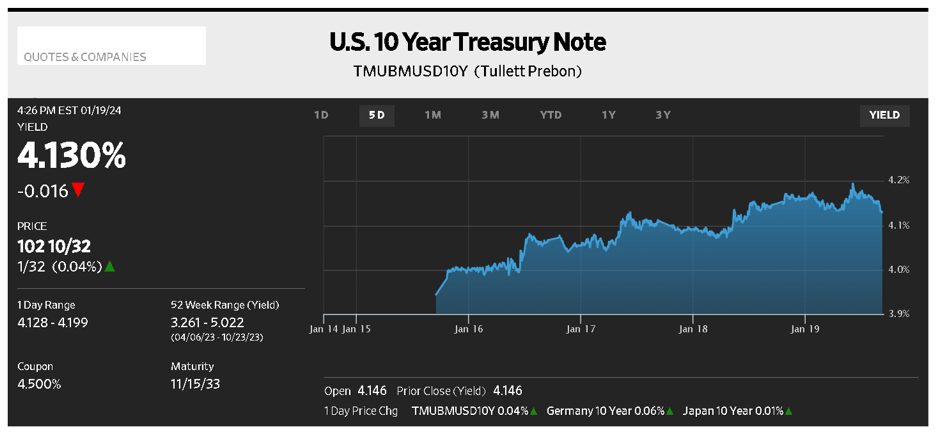

After the euphoric end to 2023 markets reversed course last week, ending a nine-week rally that saw stocks reach near record highs with this benchmark Treasury moving back above 4%. At 4.05% the market is 17 bps lower than the 504 program its December debentures.

As always, there are multiple interpretations for price action and for Treasuries there are at least two observations.

With the release of the minutes from the FOMC’s December 12-13 meeting last Wednesday the rates market began trending higher as it interpreted the release for confirmation of an end to rate hikes and the timing of rate cuts that might be slower than thought, but the text of the minutes disclosed some policy makers want a discussion on the circumstances under which their Quantitative Tightening policy can be revised. That policy put trillions of dollars into the virus affected economy with the Fed’s balance sheet soaring to $9 trillion. From that peak in May 2022 sales and maturing debt have reduced it to $7.2 trillion with a possible end to that runoff. Ending the policy would permit the bank to reinvest proceeds of maturing debt into their preferred investment of Treasuries which could partially offset the increased need for Treasury to fund the country’s $1.7 trillion budget deficit. It was that funding need in the second half of 2023 that helped push rates higher as the market had lost its biggest buyer, the Fed.

A recent survey of Treasury dealers expected an end to QT by December and speculation of earlier action is premature, but like the market front-running the Fed on rate cuts in 2023 a similar action could happen again this year.

Stronger than expected

The final push to higher rates on Friday was provided by the Non-Farm Payroll report that came in stronger than expected (216,000) while leaving the Unemployment Rate unchanged at 3.7%. For all of 2023 employers added 2.7 million jobs, lower than 2022’s total of 5.2 million but greater than the years leading up to the pandemic.

The labor market’s steady gain, coupled with the reduction in inflation is providing comfort for a soft landing to the economy which would preclude additional rate hikes. Aiding that assessment is the annualized six-month rate of core PCE inflation that fell to 1.9% last quarter.

The Week Ahead

The SBA 504 program prices its January debentures, Treasury is active with its quarterly refunding, and we get more inflation data.

Monday – Treasury sells $143 billion 13 & 26-week Bills.

Tuesday – 504 program announces its 10, 20 & 25 year debenture sale, Treasury sells $52 billion three-year Notes, Trade deficit expected to be $65 billion.

Wednesday – Treasury sells $37 billion ten-year Notes.

Thursday– 504 prices its debentures, Treasury sells $26 billion thirty-year Bonds. CPI forecast at 0.2%.

Friday – PPI forecast at 0.2%.

December 18, 2023

Commentary will resume on January 8, 2024.

December 11, 2023

The $422 million December debenture offering was sizable given the relatively short processing window and the overall backdrop in low origination/issuance activity in other lending spaces. For calendar year 2023, $5.1 billion in 504 debentures were issued. While that figure is fully $2 billion lower from the (perhaps unassailable) 2022 record, it is over $1 billion above the average of the three years before the pandemic.

Sharp m/m drop in debenture rates. CDC’s benefited from a sharp m/m drop in the debenture rates of 41 bps and 43 bps, respectively, for the 20- and 25-year maturities (rates were 5.23% and 5.28%). This is the third time in this now 45-month bear market in bonds the 504 debenture rates fell over 40 bps m/m. The prior two drops were followed by a quick resumption in the uptrend in interest rates. We must remember, this remains a bear market that no active fixed income professional has experienced.

Let’s take these m/m debenture rates drops when we can get them! Another nice note is that debenture rates now have fallen for two consecutive months, something not seen since Jul-Aug 2022.

Another “front run” attempt. The sharp drop in debenture rates from November resulted from yet another attempt by the market to push back against the Fed’s policy stance, i.e. front run the Fed. Fed leadership keeps talking Fed policy rates staying at least as high as currently and for longer. Another rate rise is on the table according to them. But the market has (again) moved forward the expected timing of the first rate cut of the next easing cycle. Back in October, using money market futures prices, the market priced a first rate cut well into the second half of 2024. Recently market pricing has that first cut moved up into the spring of 2024.